Who knows. But, as this is the time of year when lots of people who should know better start to make wild guesses, I might as well have a bit of fun and put on my Nostradamus hat (at least I have no reputation to tarnish):

My PF:

- Although you ever know when the markets will tank, I'll stick with the herd and say that the total return for the Oz stock market won't be the 20% or so we've enjoyed for the past three years, but will manage a good 10% or so. This will help my retirement fund and geared stock portfolio to have another positive year (10-20% increase).

- I imagine that commodity prices will moderate slightly as Chinese growth is held to a more sustainable rate, and oil will stay mostly within a $50-65 a barrel band in '07.

- The Sydney housing market will remain subdued (0-5% gains), despite interest rates having peaked and possibly being dropped a notch or two during '07.

- The US stock market will gain a bit by the end of '07 (5-10%), so I wouldn't be surprised if my "little book" portfolio ends up with a slight profit by the end of '07.

- At this time I'm hopeful that my NW will increase by my target 10-12% (plus my $30K savings) during the year.

World events: Hmmmm, the crystal ball is a bit cloudy, but I'd guess that:

- Nth Korea is still resisting international pressures over it's nuclear program by the end of '07, and is trying to get financial and diplomatic concessions from the US.

- China continues to build up its military and holds some impressive military exercises to intimidate Taiwan. The US gets less and less supportive of Taiwan as it's economic ties with China increase.

- Fresh elections in Palestine by the end of the year see some progress towards an negotiated peace with Israel, but sporadic violence continues to make this a long-term proposition. [Unless Israel or the US bombs some nuclear facilities in Iran during the year].

- US, Oz, UK all increase troop numbers slightly in early '07, but it's not enough to improve matters in Iraq. By the end of '07 numbers are being reduced and coalition forces are fortifying green zones and bases for maintaining a long-term presence in Iraq "supporting" the Iraqi police and army. Monthly Coalition losses start to reduce towards the end of '07, but the de facto civil war continues with civilian deaths continuing to escalate.

- Lots of wars in Africa kill lots and lots of innocent people.

- Bird Flu and Mad Cow outbreaks make headlines a couple of times, but more people are killed on the roads each day in the US, Oz, and UK than die worldwide from these two in '07.

- After considerable debate and campaigning, regulations requiring labeling of cloned meat is enacted in the US. Meanwhile people continue drop like flies from smoking, alcohol and drug abuse.

I'll give myself a score out of 12 this time next year ;)

Saturday, 30 December 2006

Friday, 29 December 2006

PPP Acquires Performancing.com

Performancing.com is a start-up focused on a Firefox Blog Editor, an Ad Network, and "Metrics" which provides statistics for Bloggers. To quote the Performancing blog from 15 Nov, Metrics is a "pro-grade blog analytics service. It currently has around 16,000 registered blogs using it, and though it's cool, it's not producing". PPP has acquired Performancing.com, Performancing Metrics and Performancing Exchange - in this deal (according to Performancing.com it does not include the Partners ad network, and does not include PFF, the free blog editor for firefox) it appears that PPP is mainly buying a "free" Metrics service that is losing money, presumably with the aim of getting a large chuck of the 16,000 bloggers using Metrics to sign-up to PPP. Having a larger blogger base should aid PPP to attract new advertisers. I can only hope that this strategy pays off, as PPP provides a nice income stream for my blog (in fact its the only signficant source of income - AdSense et al are really only worthwhile if you have a large readership). Lately the range of advertisers offering "opportunities" on PPP seems to have been diminishing - perhaps some have been scared off by the introduction of mandatory disclaimers. Also, many of the PPP advertisers are restricting their ads to blogs with high PR (which rules out blogger hosted bloggers) and requiring 200 rather than 50 word "spots" for their couple of bucks. We'll see how things develop in '07. At the moment their is a worrying increase in the number of diet, cosmetic and dating advertisers compared to those that would actually be of interest to my readers ie. financial resources.

PayPerPost

PayPerPost

Goals '07

Well, my financial goals are pretty well set and my asset allocation implemented - what actual performance I end up with this year is in the lap of the gods. So, the goals I'll be concentrating on most at the start of '07 are:

* using Quicken to track my daily transactions in detail once again [like I did before I got married, had some kids and suddenly had no spare time;) ],

* get my share transaction records up to date in Quicken so my capital gains tax calculations will be less onerous in July. It may even let me do some propoer end of tax year planning and run some "what if" scenarios.

* stick to my healthy eating plan (aka "diet") and get a bit more exercise, so I can achieve my ideal BMI by the end of June...

Aside from that I'll be busy this year doing a subject for my Masters in IT in the first half of the year, and starting my studies for a Grad Dip Ed in Secondary Science education - that will keep me busy! In the second half of the year I'm taking a leave of absence from the MIT course, as I'll be flat out with the Grad Dip Ed subjects, plus I have to do a month of prac teaching (for which I'll have to take 4 weeks annual leave from my "real" job).

It will be interesting to see where things stand at the end of '07.

* using Quicken to track my daily transactions in detail once again [like I did before I got married, had some kids and suddenly had no spare time;) ],

* get my share transaction records up to date in Quicken so my capital gains tax calculations will be less onerous in July. It may even let me do some propoer end of tax year planning and run some "what if" scenarios.

* stick to my healthy eating plan (aka "diet") and get a bit more exercise, so I can achieve my ideal BMI by the end of June...

Aside from that I'll be busy this year doing a subject for my Masters in IT in the first half of the year, and starting my studies for a Grad Dip Ed in Secondary Science education - that will keep me busy! In the second half of the year I'm taking a leave of absence from the MIT course, as I'll be flat out with the Grad Dip Ed subjects, plus I have to do a month of prac teaching (for which I'll have to take 4 weeks annual leave from my "real" job).

It will be interesting to see where things stand at the end of '07.

Shopping online for life insurance

Most financial planners will advise that you take out life, disability and possibly other insurances, or increase the amount of cover you already have. This is often good advice, as there is a larger chance of fit, young people suffering time off work (possibly indefinitely) at some stage of their working lives than many people realise, and this can have a devastating impact on your personal finances if you do not have adequate cover. Personally, I have $400K of life and TPD cover, as well as loss of income insurance (with a 12 month waiting period to reduce the cost). While it would probably not be needed if I died, as my net worth would provide a reasonable estate for my family, it would definitely be required if I suffered TPD or could not work as long as I've planned. Sudden ill health can affect any of us unexpectedly, so this is an area where it doesn't make sense to be too frugal. While you can often "self insure" and save the expense of some types of insurance - for instance comprehensive insurance on a vehicle is usually a poor "investment" once a car is several years old, it isn't possible to "self insure" for big ticket items like life insurance.

If you're shopping for insurance via a financial planner, just bear in mind that the fees generated for the planner are generally very large, and could influence their recommendations. While they often argue that "value" is more important that "cost", and it *is* very important to check all the conditions and exclusions when comparing insurance, the cost of very similar insurance products can vary considerably.

If you wish to get an idea of what the amount of insurance you have in mind would cost, you can get a lot of information online - for example, online quotes are available from financialone.com. Like most online quote providers, you have to provide your personal details in order to get a quote, so you should expect some follow up sales pitch.

If you just want some more info on life insurance, there are also some life insurance articles available, which cover topics such as:

* Smoker's Life Insurance

* Non-Smoker's Life Insurance

* Accidental Death and Dismemberment

* Waiver of Premium

* Senior's Life Insurance

* Pension Maximization

* Split Dollar Life Insurance

* Term Life Insurnace

* Irrevocable Trust Using Life Insurance

* Life Insurance for women

* Life insurance for Diabetics

* Keyman Insurance

* Life Insurance Premium Financing

Unfortunately, the trend towards rebate of up front fees for investing in mutual funds via discount brokers and fee-only financial planners doesn't seem to have spread to the insurance area of personal finances. Although it wouldn't hurt to ask your fee-only finacial planner (if you have one) for a rebate of some of the first year's insurance premium "kick back" and the trailing fees.

Financialone.com also provides a listing of the insurers that are used for their online quotations, so you can check if a particular insurer you are interested in will be included in their quotation search.

sponsored

If you're shopping for insurance via a financial planner, just bear in mind that the fees generated for the planner are generally very large, and could influence their recommendations. While they often argue that "value" is more important that "cost", and it *is* very important to check all the conditions and exclusions when comparing insurance, the cost of very similar insurance products can vary considerably.

If you wish to get an idea of what the amount of insurance you have in mind would cost, you can get a lot of information online - for example, online quotes are available from financialone.com. Like most online quote providers, you have to provide your personal details in order to get a quote, so you should expect some follow up sales pitch.

If you just want some more info on life insurance, there are also some life insurance articles available, which cover topics such as:

* Smoker's Life Insurance

* Non-Smoker's Life Insurance

* Accidental Death and Dismemberment

* Waiver of Premium

* Senior's Life Insurance

* Pension Maximization

* Split Dollar Life Insurance

* Term Life Insurnace

* Irrevocable Trust Using Life Insurance

* Life Insurance for women

* Life insurance for Diabetics

* Keyman Insurance

* Life Insurance Premium Financing

Unfortunately, the trend towards rebate of up front fees for investing in mutual funds via discount brokers and fee-only financial planners doesn't seem to have spread to the insurance area of personal finances. Although it wouldn't hurt to ask your fee-only finacial planner (if you have one) for a rebate of some of the first year's insurance premium "kick back" and the trailing fees.

Financialone.com also provides a listing of the insurers that are used for their online quotations, so you can check if a particular insurer you are interested in will be included in their quotation search.

sponsored

Happy Christmas and a Merry New Year

Wishing all my readers season's greetings. Blogger has been playing up so I'm not sure how often I'll be able to post.

Sunday, 24 December 2006

Resources Stocks Set to Crash!

Well, maybe, maybe not. I've seen a few articles about the resources boom that hold the view that when the Chinese economy and World economy takes breather (next year?) commodity prices will drop back down to their pre-boom prices as new production (stimulated by the recent profitability of resources companies) comes on stream.

A contrary view is that exploration and development was at very low levels between 1998 and 2003, so the push for increased production has only just begun. Couple this will a typical lead-time of up to 10 years to get a new mine into production and the picture for commodity prices looks somewhat more rosey.

Today's Australian Financial Review also had some interesting facts about the concentration of commodity production - a handful of big resources companies control the lion's share of production, and therefore are in a good position to maintain high commodity prices in the medium term:

I think I'll hold on to my BHP and Rio Tinto stocks for a while longer - especially as they've already come back considerably from the peaks earlier in the year.

A contrary view is that exploration and development was at very low levels between 1998 and 2003, so the push for increased production has only just begun. Couple this will a typical lead-time of up to 10 years to get a new mine into production and the picture for commodity prices looks somewhat more rosey.

Today's Australian Financial Review also had some interesting facts about the concentration of commodity production - a handful of big resources companies control the lion's share of production, and therefore are in a good position to maintain high commodity prices in the medium term:

Commodity % output from big-5

Produced in each industry

Platinum 94%

Iron Ore 85%

Nickel 82%

Alumina 55%

I think I'll hold on to my BHP and Rio Tinto stocks for a while longer - especially as they've already come back considerably from the peaks earlier in the year.

Friday, 22 December 2006

Ink Cartridges

These days its cheap enough to get print digital photos printed, but if you have just one or two pics to print it's still worth printing on your inkjet at home. If you need ink cartridges inkers has a large selection of inkjet cartridges to choose from.

I find that for most printing plain old photocopier paper works quite well, but for the odd photo you want to print at home it's best to use the proper glossy photo paper. One thing I like about inkers is that they accept payment via paypal, so you can easily use some of the money you've earned blogging to pay for your printer needs, without first having to move funds from your paypal account into a normal bank account to withdraw.

sponsored

I find that for most printing plain old photocopier paper works quite well, but for the odd photo you want to print at home it's best to use the proper glossy photo paper. One thing I like about inkers is that they accept payment via paypal, so you can easily use some of the money you've earned blogging to pay for your printer needs, without first having to move funds from your paypal account into a normal bank account to withdraw.

sponsored

96 1/4% OFF!

I got an email from wealthcreator.com.au a few days ago announcing the launch of their "investment shop". The email included a $15 evoucher as a Christmas gift. So I checked out what was on "special" and found that the "The Bullseye Investment System, - Audio Tapes & WorkBook" was on clearance sale for $24.00 (RRP $240). After applying the discount this ended up costing me just $9.00 (there's free shipping on courseware, presumably because the profit margin is usually quite large on these products) - a 96.25% "saving".

The "Bullseye Investment System" course comes on 6 audio cassettes (my car doesn't have a CD player), so it will be good to listen to on the 1-hour drive to or from work. According to the marketing guff "The Bullseye System is designed to help eliminate poor investment choices, identify superior investment opportunities, maximize profit potential, minimize risk, and simplify portfolio monitoring."

The "Bullseye Investment System" course comes on 6 audio cassettes (my car doesn't have a CD player), so it will be good to listen to on the 1-hour drive to or from work. According to the marketing guff "The Bullseye System is designed to help eliminate poor investment choices, identify superior investment opportunities, maximize profit potential, minimize risk, and simplify portfolio monitoring."

Wednesday, 20 December 2006

Home Equity Loans

Home Equity Loans, like all debt, need to be used responsibly. I've used a home equity loan to borrow funds to invest in my "Little Book" US Shares portfolio (actually, if you read the information available on the personalhomeloanmortgages.com website, what I've got is called a HELOC in the US, rather than a home equity loan). After establishing how much home equity I had, I established a loan account and use this to fund each month's investment of $5000 worth of the particular stock I've chosen using the "Little Book" website. After 18 months I'll be fully invested with a loan balance of around $90,000 secured against my home equity. The stock dividends will help pay the loan interest, and, if all goes according to plan, the investment value will increase at a greater rate than the interest rate on the home equity loan. As with all types of borrowing to invest (aka "gearing" or "leverage") your gains or losses will be magnified by using "other people's money [OPM]" to invest, and you need to thoroughly "stress test" your plans against possible interest rate changes (if you use a variable rate loan), and problems such as ill health or unemployment.

PayPerPost

PayPerPost

Sunday, 17 December 2006

US Shares - "Little Book" Portfolio Update: Dec 06

My "Little Book that Beats the Market" Portfolio had a poor month, with several of the stocks dropping significantly. As my version of the "Little Book" strategy is to hold each stock for 18 months after purchase, then sell it and replace it with a new pick (unless its still in the short list), the monthly valuations won't really mean anything during the accumulation phase. Even once I start "rolling over" my holdings the annual returns won't show how well this strategy is performing - as it's meant to be a long term strategy. Hopefully after ten years I'll have some idea if it's achieving the target ROI of 15%. As this portfolio is being built entirely with borrowed funds, the ROI has to at least exceed the loan interest rate (around 8%) to be considered a "success" in the long run).

One reader has asked if this portfolio is hedged - the answer is "no" as I have no idea if the AUD will rise or fall vs. the USD over the long term (10+ years), and I'm not going to complicate things further by trying to guess the short term currency movements. Hedging without trying to actively "trade" currencies would just add another 1%+ pa to the costs of running this portfolio in the long term.

TRANSACTIONS THIS MONTH

BOUGHT: 300 shares in OMNIVISION TECHNOLOGIES [OVTI] on 13 Nov @ $16.47 - total cost USD$5,006.00 including $65 brokerage.

BOUGHT: 320 shares in EQIP SYSTEMS [EPIQ] on 11 Dec @ $15.65 - total cost USD$5,073.00 including $65 brokerage.

SOLD: No sale this month (portfolio is in accumulation phase - US$5,000 purchase each month for 18 months)

When selecting which stocks to buy I've been keeping clear of commodity (mining & oil) stocks as I think the "e" in their p/e rations may start declining within the next 18 months if commodity prices moderate as production increases meet demand.

PORTFOLIO PERFORMANCE:

I'm currently ahead by 6.86% (AUD$3,109.52) after deducting an additional $65 per stock holding for selling costs, but not allowing for loan interest expenses or dividends received.

nb. The average gain reported above is spurious as each stock has a different holding period, and the current prices have been automatically converted into AUD, while the buy/sell commissions I entered into Yahoo! portfolio haven't been converted. I'll start tracking ROI more accurately once I'm fully invested at the end of the first 18 months.

One reader has asked if this portfolio is hedged - the answer is "no" as I have no idea if the AUD will rise or fall vs. the USD over the long term (10+ years), and I'm not going to complicate things further by trying to guess the short term currency movements. Hedging without trying to actively "trade" currencies would just add another 1%+ pa to the costs of running this portfolio in the long term.

TRANSACTIONS THIS MONTH

BOUGHT: 300 shares in OMNIVISION TECHNOLOGIES [OVTI] on 13 Nov @ $16.47 - total cost USD$5,006.00 including $65 brokerage.

BOUGHT: 320 shares in EQIP SYSTEMS [EPIQ] on 11 Dec @ $15.65 - total cost USD$5,073.00 including $65 brokerage.

SOLD: No sale this month (portfolio is in accumulation phase - US$5,000 purchase each month for 18 months)

When selecting which stocks to buy I've been keeping clear of commodity (mining & oil) stocks as I think the "e" in their p/e rations may start declining within the next 18 months if commodity prices moderate as production increases meet demand.

PORTFOLIO PERFORMANCE:

I'm currently ahead by 6.86% (AUD$3,109.52) after deducting an additional $65 per stock holding for selling costs, but not allowing for loan interest expenses or dividends received.

Symbol 52-wk Range P/E Trade Shrs Trade Date Price Paid Commission Holdings Value Gain

HRB 19.80 - 25.75 24.95 23.55 200 28-Jun-06 24.16 130.00 $6,029.57 -286.18Down $286.18 Down 4.53%

MOT 18.66 - 26.30 12.35 20.71 265 24-Jul-06 18.98 130.00 $7,025.73 456.89Up $456.89 Up 6.96%

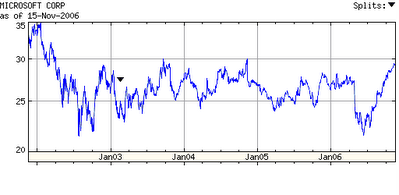

MSFT 21.46 - 30.23 24.13 30.19 200 21-Aug-06 24.64 130.00 $7,729.63 1,290.98Up $1,290.98 Up 20.05%

ASEI 36.03 - 93.86 26.89 65.81 100 18-Sep-06 49.51 130.00 $8,424.76 1,956.67Up $1,956.67 Up 30.25%

PWEI 18.15 - 38.16 4.32 34.75 150 13-Oct-06 33.29 130.00 $6,672.85 150.36Up $150.36 Up 2.31%

OVTI 13.45 - 34.49 11.09 14.49 300 13-Nov-06 16.47 130.00 $5,565.03 -890.42Down $890.44 Down 13.79%

EPIQ 14.31 - 23.40 8.52 17.02 320 11-Dec-06 15.65 130.00 $6,972.29 431.22Up $431.22 Up 6.59%

Total (AUD): - - - - - - - $48,419.86 3,109.52Up $3,109.50 Up 6.86%

nb. The average gain reported above is spurious as each stock has a different holding period, and the current prices have been automatically converted into AUD, while the buy/sell commissions I entered into Yahoo! portfolio haven't been converted. I'll start tracking ROI more accurately once I'm fully invested at the end of the first 18 months.

Saturday, 16 December 2006

Found money

DW thinks I have a "gift" for spotting lost coins - whenever we're walking along the footpath and there's a coin lying on the ground, invariably I'm the one that spots the coin. Today I was throwing out some trash at the food court and spotted 25c change someone had left with their rubbish on the takeaway food tray. Another contribution to DS1's money box ;) It got me wondering just how much loose change is discarded by mistake and ends up in the land fill every day.

Scams, shams and shame

I always love reading about a good scam - luckily I've never* been sucked in myself by one of these dodgy schemes, and the more of them you read about, the better you get at picking them. A good listing of some of the more common scams is here.

* Well, I did almost sent in some of my Paypal account details once in response to an phishing email - there are lots of emails purporting to be from Paypal that either request you to "confirm" your account details, "reactivate" your account, or pretend that your paypal account has paid some money to a company you've never heard of. In each case, they're just phishing for you account info. Unfortunately, these emails often look just like a real Paypal email, complete with the corrects fonts, content, layout, logos etc. and although you can often tell by the senders address, or the URL links to (such as http://paypal.dodgyco.com/paypal.htm) sometimes it's very hard to tell without some higher level internet snooping ability. These days I just ignore ALL emails that purport to be from paypal, which means I never get to read any newsletters or official notification emails. I really wish that email was NOT free - if there was a small charge (say 5c) to send an email, 99.9% of all spam and phishing emails would disappear as it wouldn't be profitable any more.

* Well, I did almost sent in some of my Paypal account details once in response to an phishing email - there are lots of emails purporting to be from Paypal that either request you to "confirm" your account details, "reactivate" your account, or pretend that your paypal account has paid some money to a company you've never heard of. In each case, they're just phishing for you account info. Unfortunately, these emails often look just like a real Paypal email, complete with the corrects fonts, content, layout, logos etc. and although you can often tell by the senders address, or the URL links to (such as http://paypal.dodgyco.com/paypal.htm) sometimes it's very hard to tell without some higher level internet snooping ability. These days I just ignore ALL emails that purport to be from paypal, which means I never get to read any newsletters or official notification emails. I really wish that email was NOT free - if there was a small charge (say 5c) to send an email, 99.9% of all spam and phishing emails would disappear as it wouldn't be profitable any more.

Wednesday, 13 December 2006

Frugal living: Birthday Cards

As it's my birthday I decided to try out the birthday content available on American Greetings website. They have a wide selection of ecards, invitations, and printables as well as the reminder service available to keep track of birthdays of family and friends, and some of the ecards are free. Compared to paying for a printed card and postage this will save several dollars for each card you send. I used to buy $1 cards at a discount shop, but this still ends up costing $1.50 (with postage) for something that ends up in the bin a few days after it's been received. Now that nearly all my friends and relatives have an email address, the ecard is a real winner.

The free reminder service and desktop calendar available on the website is also great for keeping track of birthdays and making sure you don't forget an important birthday ever again. There is a range of cards available covering such categories as:

# Belated

# Family

# Friends

# Funny

# Just For Her

# Just For Him

# Just For Kids

# Romantic

# Characters You Love

# Milestone

# Over The Hill

# Religious

# Co-workers

# Holiday Birthdays

# Pets

and most categories have at least one free ecard available.

PayPerPost

The free reminder service and desktop calendar available on the website is also great for keeping track of birthdays and making sure you don't forget an important birthday ever again. There is a range of cards available covering such categories as:

# Belated

# Family

# Friends

# Funny

# Just For Her

# Just For Him

# Just For Kids

# Romantic

# Characters You Love

# Milestone

# Over The Hill

# Religious

# Co-workers

# Holiday Birthdays

# Pets

and most categories have at least one free ecard available.

PayPerPost

Happy Birthday to Me!

Well, today was my birthday. Overall it was an enjoyable day and fairly economical day. I had the day off work (my company gives everyone an extra day of "birthday leave" each year, which is very nice of them), and I spent the morning driving DS1 to an appointment at the Children's hospital for a check-up with his immunologist (he has food allergies and eczema). As the specialist consult and "skin-prick" allergy testing was all covered by medicare, this didn't cost me anything (Well, technically my 1.5% medicare tax levy paid for it). There will be some out of pocket expense for his latest medications, but not today ;)

I had some bread rolls and turkey slices from the supermarket for lunch ($9.89) - but there's about half the turkey and bread rolls left over to take for lunch at work tomorrow, so it was fairly economical.

We then visited the Borders bookstore and browsed through a few books after lunch. My wife had a coffee and I ended up buying a $9.95 science book as another Christmas present for DS1, so this wasn't as cheap entertainment as it usually is. On the way home we dropped by my parents so they could say "happy birthday" and Mum gave me another birthday gift (a back-support car seat cover - at least it's useful). My parents had previously already given me a book, a 1oz silver coin (which I'd asked for) and an electronic knick-knack (a "joke master" - which I'll probably never use) for my birthday. DW gave me a wipe-off 2007 calendar as a token gift, which will also be of use.

Dinner was a pork fillet and some pumpkin, plus a couple more of the bread rolls from lunch. Next will be some free-to-air TV (Numb3rs and Survivor) before an early night (we have to leave early tomorrow for DS1's recorder concert rehearsal before school).

As my net worth has been bobbing *just* over the $1M mark this week, this is how a "millionaire" spends his birthday!

I had some bread rolls and turkey slices from the supermarket for lunch ($9.89) - but there's about half the turkey and bread rolls left over to take for lunch at work tomorrow, so it was fairly economical.

We then visited the Borders bookstore and browsed through a few books after lunch. My wife had a coffee and I ended up buying a $9.95 science book as another Christmas present for DS1, so this wasn't as cheap entertainment as it usually is. On the way home we dropped by my parents so they could say "happy birthday" and Mum gave me another birthday gift (a back-support car seat cover - at least it's useful). My parents had previously already given me a book, a 1oz silver coin (which I'd asked for) and an electronic knick-knack (a "joke master" - which I'll probably never use) for my birthday. DW gave me a wipe-off 2007 calendar as a token gift, which will also be of use.

Dinner was a pork fillet and some pumpkin, plus a couple more of the bread rolls from lunch. Next will be some free-to-air TV (Numb3rs and Survivor) before an early night (we have to leave early tomorrow for DS1's recorder concert rehearsal before school).

As my net worth has been bobbing *just* over the $1M mark this week, this is how a "millionaire" spends his birthday!

How Much Money

NCN did an interesting post that listed how much he had earned so far, and how much he could have saved up by now (if he'd saved 10% of his income every year) compared to what he's actually accumulated (starting a couple of years ago).

I thought I'd run through the same process myself, just for interest:

"How much money have I made during my lifetime."

Here are the details. I'm almost 45, and I've worked since I was about 14 (part-time during high-school doing a paper round, market gardening, storeman & packer and music tutor, and then during uni vacations working in a pencil factory). The breakdown:

These are rather rough estimates (but pretty close) for the early years. I got my first "real" job in 1984 working as an "engineering trainee" while finishing off my first degree.

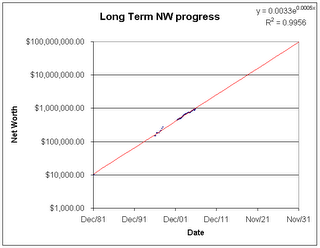

So, how much money have I made, in salary, over the past 32 years? $935,719. Now, for some folks, that's not much money, and for others, it's a lot of money. Whatever you think about the amount you have to admit that it is a pretty decent chunk of change. To continue with NCN's method of analysis... Where would I be if I had SAVED 10 percent of my salary, at say 8 percent interest, per year. And how does this compare to where I'm actually at. Let's run the numbers:

At the end of the 32 year period, I would have had 220,152.18 in my retirement account. Not bad. Instead, I have about 304K, as I've been putting in more than 10% and have averaged more than 8% by investing in the "high growth" funds available in my retirement account. Now, for the sobering reality. Ready? If I NEVER put another dollar into retirement, but left that 304K to grow at 8 percent, how much money would I have in, say, 20 years when I'm ready to retire?

Over $1,026,000.

Yep, that's right. I've saved around 10 per cent of my income while working, and in another 20 years I should have over $1,000,000 dollars in my retirement account, without ever saving another cent.

Wow! Now, as you can see, I have "low-balled" my estimates. I assumed a VERY modest amount of savings, and a very, very modest rate of return, which is why I actually have 38% more in my retirement account than this model predicts. If I just stick with the conservative 8% return and don't contribute any more I STILL would have over 1 MILLION dollars in my retirement account. This shows how important time is.

In reality, I'm now saving around 20% of my salary into my retirement account and will continue to do so. Assuming I earn to same amount for the next 5 years and then take a pay cut when I take up a high school science teaching job, I'll end up with $1,401,207 at 65. The recent Australian tax changes mean that my retirement account earnings are only taxed at 15% and the final benefit, taken as either a lump sum or a pension, will be tax free. So this should be enough for a comfortable retirement. In fact, based on my current spending and the fact that I won't have a mortgage when I retire, I'll probably have more income than I need and will be able to increase my savings rate when I'm "retired". I suppose at that time I'll have to consider myself a "professional" investor. After I've completed my teaching qualification and Master of IT I may enrol in the Master of Finance course my wife is currently doing so I can officially call myself a "pro" ;)

My other assets (around $700K) will continue to be invested in real estate and stocks, even after I retire, so this should provide a sizeable estate for my two sons and their heirs. I've already set up retirement accounts for each of them, so they should end up with a comfortable retirement even if they never contribute anything to their retirement accounts.

It's amazing what you can achieve on a "modest" salary via a regular savings plan and sensible investments over the long haul.

I thought I'd run through the same process myself, just for interest:

"How much money have I made during my lifetime."

Here are the details. I'm almost 45, and I've worked since I was about 14 (part-time during high-school doing a paper round, market gardening, storeman & packer and music tutor, and then during uni vacations working in a pencil factory). The breakdown:

Year Salary

1974 200

1975 300

1976 400

1977 500

1978 1000

1980 2000

1981 2000

1982 2000

1983 5000

1984 14000

1985 16000

1986 18000

1987 20000

1988 22000

1989 24440

1990 27926

1991 31985

1992 34695

1993 37678

1994 38509

1995 38924

1996 38924

1997 40481

1998 41695

1999 39047

2000 40286

2001 55714

2002 58093

2003 66261

2004 68249

2005 73602

2006 75810

These are rather rough estimates (but pretty close) for the early years. I got my first "real" job in 1984 working as an "engineering trainee" while finishing off my first degree.

So, how much money have I made, in salary, over the past 32 years? $935,719. Now, for some folks, that's not much money, and for others, it's a lot of money. Whatever you think about the amount you have to admit that it is a pretty decent chunk of change. To continue with NCN's method of analysis... Where would I be if I had SAVED 10 percent of my salary, at say 8 percent interest, per year. And how does this compare to where I'm actually at. Let's run the numbers:

Ten Percent End Of Year

20 21.60

30 55.73

40 103.39

50 165.66

100 286.91

200 525.86

200 783.93

200 1,062.65

500 1,687.66

1,400 3,334.67

1,600 5,329.44

1,800 7,699.80

2,000 10,475.78

2,200 13,689.85

2,444 17,424.55

2,793 21,834.53

3,199 27,035.67

3,470 32,945.58

3,768 39,650.45

3,851 46,981.46

3,892 54,943.77

3,892 63,543.06

4,048 72,998.46

4,170 83,341.39

3,905 94,225.78

4,029 106,114.73

5,571 120,621.02

5,809 136,544.75

6,626 154,624.51

6,825 174,365.37

7,360 196,263.61

7,581 220,152.18

At the end of the 32 year period, I would have had 220,152.18 in my retirement account. Not bad. Instead, I have about 304K, as I've been putting in more than 10% and have averaged more than 8% by investing in the "high growth" funds available in my retirement account. Now, for the sobering reality. Ready? If I NEVER put another dollar into retirement, but left that 304K to grow at 8 percent, how much money would I have in, say, 20 years when I'm ready to retire?

Over $1,026,000.

Yep, that's right. I've saved around 10 per cent of my income while working, and in another 20 years I should have over $1,000,000 dollars in my retirement account, without ever saving another cent.

Wow! Now, as you can see, I have "low-balled" my estimates. I assumed a VERY modest amount of savings, and a very, very modest rate of return, which is why I actually have 38% more in my retirement account than this model predicts. If I just stick with the conservative 8% return and don't contribute any more I STILL would have over 1 MILLION dollars in my retirement account. This shows how important time is.

In reality, I'm now saving around 20% of my salary into my retirement account and will continue to do so. Assuming I earn to same amount for the next 5 years and then take a pay cut when I take up a high school science teaching job, I'll end up with $1,401,207 at 65. The recent Australian tax changes mean that my retirement account earnings are only taxed at 15% and the final benefit, taken as either a lump sum or a pension, will be tax free. So this should be enough for a comfortable retirement. In fact, based on my current spending and the fact that I won't have a mortgage when I retire, I'll probably have more income than I need and will be able to increase my savings rate when I'm "retired". I suppose at that time I'll have to consider myself a "professional" investor. After I've completed my teaching qualification and Master of IT I may enrol in the Master of Finance course my wife is currently doing so I can officially call myself a "pro" ;)

My other assets (around $700K) will continue to be invested in real estate and stocks, even after I retire, so this should provide a sizeable estate for my two sons and their heirs. I've already set up retirement accounts for each of them, so they should end up with a comfortable retirement even if they never contribute anything to their retirement accounts.

It's amazing what you can achieve on a "modest" salary via a regular savings plan and sensible investments over the long haul.

Monday, 11 December 2006

PPP blog Makes an Interesting Read

Having been a "postie" for quit a while now, it's interesting to learn a bit about what goes on "behind the scenes" at PayPerPost. Now you can get a peek via their blog and get a look at the current PPP news, updates and crazy videos.

Even if you're not a PPP "postie" I think it's interesting to see what is happening day-to-day at such an internet startup company. The recent posts cover topics such as their recent server upgrade, how search engines treat links embedded within sponsored posts, and some recent videos. The archives go back to the mists of time - June '06 in fact.

PayPerPost

Even if you're not a PPP "postie" I think it's interesting to see what is happening day-to-day at such an internet startup company. The recent posts cover topics such as their recent server upgrade, how search engines treat links embedded within sponsored posts, and some recent videos. The archives go back to the mists of time - June '06 in fact.

PayPerPost

Net Worth - PF Bloggers progress for NOV '06

Here's the regular round up on how the various PF bloggers who post Net Worth each month are progressing.

Leave a comment if I've missed yours out!

nb. Some ages have been adjusted as follows:

exact age provided = listed as given

"20's" = listed as 2x

"early 20's" = listed as 22

"mid-late 20's" = listed as 27

and so on.

Leave a comment if I've missed yours out!

Monthly Net Worth of PF Bloggers for NOV 2006:

Blogger Age Net Worth $ Change % Change

Accumulating Money 2x $43,141.79 $2,732.33 6.8%

Consumerism Commentary 30 $67,376.57 $3,536.90 5.5%

Enough Wealth 44 $991,692.00 $686.00 0.1%

Financial Freedom 30 no Nov data no Nov data N/A

Ima Saver 6x $1,376,481.00 N/A N/A

It's Just Money 32 $152,126.94 $1,611.45 1.1%

Lazy Man and Money 2x $181,501.19 N/A N/A

Make love, not debt 2x -$74,995.01 $1,816.84 2.4%

Making Our Way 37 $613,426.28 $4,961.04 0.8%

Mapgirl 32 $33,602.00 -$921.00 -2.7%

My Money Blog 28 $119,111.00 $5,127.00 4.5%

My Money Path 29 $102,480.00 $2,220.00 2.2%

My Open Wallet 37 no Nov data no Nov data N/A

New Age Personal Finance 31 $142,106.77 $8,922.50 6.7%

Savvy Saver 27 $217,449.00 $4,130.00 1.9%

nb. Some ages have been adjusted as follows:Blogger Age Net Worth $ Change % Change

Accumulating Money 2x $43,141.79 $2,732.33 6.8%

Consumerism Commentary 30 $67,376.57 $3,536.90 5.5%

Enough Wealth 44 $991,692.00 $686.00 0.1%

Financial Freedom 30 no Nov data no Nov data N/A

Ima Saver 6x $1,376,481.00 N/A N/A

It's Just Money 32 $152,126.94 $1,611.45 1.1%

Lazy Man and Money 2x $181,501.19 N/A N/A

Make love, not debt 2x -$74,995.01 $1,816.84 2.4%

Making Our Way 37 $613,426.28 $4,961.04 0.8%

Mapgirl 32 $33,602.00 -$921.00 -2.7%

My Money Blog 28 $119,111.00 $5,127.00 4.5%

My Money Path 29 $102,480.00 $2,220.00 2.2%

My Open Wallet 37 no Nov data no Nov data N/A

New Age Personal Finance 31 $142,106.77 $8,922.50 6.7%

Savvy Saver 27 $217,449.00 $4,130.00 1.9%

exact age provided = listed as given

"20's" = listed as 2x

"early 20's" = listed as 22

"mid-late 20's" = listed as 27

and so on.

Sunday, 10 December 2006

Rental Property Blues (cont.)

Finally a new tenant has been found for our investment property - the rent was lowered back to the previous rate ($400 per week), so this means that we haven't raised the rent for a couple of years now. It's more important to have a tenant than hold out for an extra $10 a week. The new tenants have only signed a 6 month lease, but will stay on thereafter on an ongoing basis (4 weeks notice is required to terminate after the lease period ends). I'm hopeful that they may stay for several years as they have no kids (yet) and seem happy enough with the property and location.

My wife seems to have lost a bit of interest in being a "landlord" now that the property market has been stagnant for a couple of years, and because having no tenants for over three months was stretching our finances a bit. She was also a bit shocked by the costs of plumbing repairs and getting the place recarpeted and new kitchen lino last year (even though I meet all the "miscellaneous" costs of this investment - we just split the loan repayments 50:50).

The "experts" in the local papers are predicting rents will increase 5%-10% in Sydney over the next 12 months due to more people renting due to high property prices and a drop off in the construction of new housing due to the lack of capital gains in the past couple of years. We only just took out a 5 year fixed rate loan for the investment property last year (the variable rate is already higher than the fixed rate we got, so this will probably work out well for this 5 year term), so we won't be looking to sell the property for at least 4 years. Hopefully by then rents will have picked up and interest rates dropped a bit which should rekindle interest in property investment and trigger some price appreciation. The long term rate of price appreciation in Sydney is around 6% pa, so hopefully after two years of flat or decreasing prices, we may see a gain of 20%-30% from present levels by the time we want to sell the property in '11 or thereabouts.

If we do sell the investment property I'll be happy to invest in property via listed property trusts in future.

My wife seems to have lost a bit of interest in being a "landlord" now that the property market has been stagnant for a couple of years, and because having no tenants for over three months was stretching our finances a bit. She was also a bit shocked by the costs of plumbing repairs and getting the place recarpeted and new kitchen lino last year (even though I meet all the "miscellaneous" costs of this investment - we just split the loan repayments 50:50).

The "experts" in the local papers are predicting rents will increase 5%-10% in Sydney over the next 12 months due to more people renting due to high property prices and a drop off in the construction of new housing due to the lack of capital gains in the past couple of years. We only just took out a 5 year fixed rate loan for the investment property last year (the variable rate is already higher than the fixed rate we got, so this will probably work out well for this 5 year term), so we won't be looking to sell the property for at least 4 years. Hopefully by then rents will have picked up and interest rates dropped a bit which should rekindle interest in property investment and trigger some price appreciation. The long term rate of price appreciation in Sydney is around 6% pa, so hopefully after two years of flat or decreasing prices, we may see a gain of 20%-30% from present levels by the time we want to sell the property in '11 or thereabouts.

If we do sell the investment property I'll be happy to invest in property via listed property trusts in future.

Friday, 8 December 2006

Free Credit Report

The free credit report I'd requested on 31st October still hadn't arrived, so I rang up Baycorp to check. After confirming my details the CSR advised that it had been emailed on the 9th November (funny how to free report which can "take up to 10 days" to send, was emailed EXACTLY 10 days after I'd faxed in my request). As I hadn't received the report I asked the CSR to check what email address they had sent it to - sure enough, even though my email address had been printed clearly in block letters they had managed to data enter a typo and send the report to some other address (Hopefully that email address is not in use by anyone - the password security on the emailed report is simply to enter my DOB, which I'm sure is available online somewhere).

As it was their stuff up, the CSR promised to immediately despatch a new report, and it turned up in my email about 10 minutes later. The end result was that ended up getting a free copy of the "premium" report (normally $27). There's not much to the report - as I haven't made any late payments there was only my current and previous address, and a list of 12 credit enquiries made over the past 5 years or so. It all looked pretty much as expected. I certainly wouldn't bother paying for this report.

As it was their stuff up, the CSR promised to immediately despatch a new report, and it turned up in my email about 10 minutes later. The end result was that ended up getting a free copy of the "premium" report (normally $27). There's not much to the report - as I haven't made any late payments there was only my current and previous address, and a list of 12 credit enquiries made over the past 5 years or so. It all looked pretty much as expected. I certainly wouldn't bother paying for this report.

Tuesday, 5 December 2006

Frugal living: Free Computer Desktop Wallpapers

If you get bored with your current desktop wallpaper definitely don't go out and pay good money for such software - you can get good quality computer desktop wallpaper's for free. American Greetings has a wide selection of free desktop wallpaper. The selection can be viewed online and are easy to download - you will be asked to provide some personal information such as your name, birthdate and email address, but that information isn't distributed to other parties and you can opt-out of receiving any newsletters from American Greetings during the sign up process. The wallpapers contain no spyware or adware (unlike other popular wallpapers and screensavers sites) and there are screensavers available as well.

The categories and individual wallpapers offered include;

* Calendars

* Floral

* Pets

* Animals

* Abstract Designs

* Graphic Patterns

* Inspirational (Religous, not business)

* Nature Scenes

* Vacation Photos

* Scenic Paintings

* Holidays

* Seasonal

* Patriotic (USA)

* General

* Children's Characters

PayPerPost

The categories and individual wallpapers offered include;

* Calendars

* Floral

* Pets

* Animals

* Abstract Designs

* Graphic Patterns

* Inspirational (Religous, not business)

* Nature Scenes

* Vacation Photos

* Scenic Paintings

* Holidays

* Seasonal

* Patriotic (USA)

* General

* Children's Characters

PayPerPost

Electronic Statements

I've been a fan of electronic bill payments (either using my CC on the phone or interet, or using bPay to direct debit my bank account) since it became available. But I must admit that electronic bills and statements have never appealed to me. Using free email accounts from netscape or yahoo means that there's always a danger that your emailed statements may disappear - especially using netscape, where your emails get deleted if you don't access your account for 30 days. Also, having to print them out to file them could cost me time and money - whereas getting the paper ones mailed to me costs them money.

So, as most electronic statements (dividends, bank statements etc) would be emailed to you I've always said "no thanks" - up to now. However, I may accept the electronic statement offer I recently got from ING. Firstly, they will store your statements on their site (permanently according to their ad), so I can access it any time via the 'net, and if my electronic statements ever went missing they should retrieve my data for me at no cost (since it's stored on their server).

The second reason is that they currently have a competition for converting to electronic statements - with three $2000 prizes up for grabs.

So, as most electronic statements (dividends, bank statements etc) would be emailed to you I've always said "no thanks" - up to now. However, I may accept the electronic statement offer I recently got from ING. Firstly, they will store your statements on their site (permanently according to their ad), so I can access it any time via the 'net, and if my electronic statements ever went missing they should retrieve my data for me at no cost (since it's stored on their server).

The second reason is that they currently have a competition for converting to electronic statements - with three $2000 prizes up for grabs.

Monday, 4 December 2006

Net Worth Update: Dec 06

The past month ended up flat with good gains in my stock portfolio and retirement account being offset by a drop in the valuations of my real estate assets:

* Average property prices decreased, dropping my property equity by $19,155 or 2.60%,

* My stock portfolio equity went up another $21,865 (7.25%) and my retirement account also increased slightly - by $335 to $301,981 (up 0.11%).

My Networth as at 30 Nov now totals $991,692 (AUD), an overall increase of just 0.07%.

I doubt that I will break through A$1,000,000 before the end of this year - property could go either up or down, and my US share funds are getting impacted by the decline in the USD vs. AUD.

personal finance, investment, wealth, stocks, real estate, saving

* Average property prices decreased, dropping my property equity by $19,155 or 2.60%,

* My stock portfolio equity went up another $21,865 (7.25%) and my retirement account also increased slightly - by $335 to $301,981 (up 0.11%).

My Networth as at 30 Nov now totals $991,692 (AUD), an overall increase of just 0.07%.

I doubt that I will break through A$1,000,000 before the end of this year - property could go either up or down, and my US share funds are getting impacted by the decline in the USD vs. AUD.

personal finance, investment, wealth, stocks, real estate, saving

Time is Money

One of the most common (and easily fixed) reasons people give for not getting ahead financially is that they "don't have enough time" to spend on managing their money and putting together a sensible financial plan. Indeed, I've read that most people spend more time planning their annual vacation than they do on planning and managing their finances. If you're "time poor", and wish to improve your time management skills so you can spend more time on money management, check out the free pdf book on basic time management skills available from timethoughts.com

Their eBook includes information on:

* Taking control of your projects and tasks

* Setting priorities and focus on what is most important

* Building and using a to-do list

* Overcoming procrastination

* Making time for the things that really matter to you

* Managing your email effectively and emptying your Inbox

* Using weekly planning to balance important and urgent tasks

* Creating an effective filing system

* Making meetings work

* Eliminating useless and low priority work from your schedule

* Delegating tasks effectively

* Getting your workload under control

You just have to find and click on the "take our online time management course" link - there are a lot of other links on the page which lead to ads for the $29.95 eBook or to sign-up for their newsletter.

PayPerPost

Their eBook includes information on:

* Taking control of your projects and tasks

* Setting priorities and focus on what is most important

* Building and using a to-do list

* Overcoming procrastination

* Making time for the things that really matter to you

* Managing your email effectively and emptying your Inbox

* Using weekly planning to balance important and urgent tasks

* Creating an effective filing system

* Making meetings work

* Eliminating useless and low priority work from your schedule

* Delegating tasks effectively

* Getting your workload under control

You just have to find and click on the "take our online time management course" link - there are a lot of other links on the page which lead to ads for the $29.95 eBook or to sign-up for their newsletter.

PayPerPost

Free Online Financial Planning Program

A group of charities has banded together to recommend people use a free online financial planning program called MoneyMinded that has helped 15,000 Australians gain control of their finances. A recent evaluation by RMIT University found that 93 per cent of those who used it had changed their spending habits, drawn up a budget or made other positive changes.The charities are urging people to complete the program's 45-minute planning and saving course that showed how to make a family money plan. Among other things the program helps people differentiate "between items they need and items they want when shopping". Such education is desperately needed by low and middle income families - a recent survey of 400 Sydney families by Wesley Mission found almost one in four had never prepared a budget.

Sunday, 3 December 2006

Estimating your real estate equity

Real estate equity is just as much a part of your net worth as your stocks, bonds, cash and retirement accounts - especially if you own any investment properties. Although you can't get daily closing prices like you can with stocks, it is possible to get information that allows you to estimate your properties current valuation.

One such source of information is eppraisal.com which provides property appraisal information. It's very quick and easy to use - I tested it with my Sister-in-Law's address in the USA and got a valuation estimate in less than 10 seconds:

Estimated Value Range: $201,157 - $334,134

Eppraisal for: nnn XXXXX Dr, Liberty, MO 64068

As they state on the website, the estimate has a large range due to it being based on recent sales in the area, but lacking specific details of the property being "eppraised". So, in order to use this data to track your own property, it would be best if you could calibrate the estimate by comparing the mid-point of the valuation range with an actual sale price (if you start tracking your property from the time you buy it), or else get a "real" appraisal done as a one off, and use that valuation to calibrate the eppraisal valuation, which could then be refreshed monthly to keep your net worth data up to date.

PayPerPost

One such source of information is eppraisal.com which provides property appraisal information. It's very quick and easy to use - I tested it with my Sister-in-Law's address in the USA and got a valuation estimate in less than 10 seconds:

Estimated Value Range: $201,157 - $334,134

Eppraisal for: nnn XXXXX Dr, Liberty, MO 64068

As they state on the website, the estimate has a large range due to it being based on recent sales in the area, but lacking specific details of the property being "eppraised". So, in order to use this data to track your own property, it would be best if you could calibrate the estimate by comparing the mid-point of the valuation range with an actual sale price (if you start tracking your property from the time you buy it), or else get a "real" appraisal done as a one off, and use that valuation to calibrate the eppraisal valuation, which could then be refreshed monthly to keep your net worth data up to date.

PayPerPost

Saturday, 2 December 2006

Bad Health, Bad Wealth

An article in the NYT discusses the costs of being overweight - not just on your health but in cold, hard cash. For example, an extra 36 grams of fat tissue is estimated to add to future medical costs in the order of $6.64 for an obese man and $3.46 for an obese woman.

Moreover, research has shown that employers discriminate against overweight people - probably because they do not want to be burdened with higher health insurance costs, or possibly just because they believe the obese are lazy, weak-willed or considered too unattractive to interact with customers. Reaerch by John H. Cawley, of Cornell University, found that a weight increase of 64 pounds above the average for white women was associated with 9 percent lower wages.

The obese accumulate only about half the assets of the normal-size American - for every one-point increase in BMI index, net worth dropped by $1,000. The typical female baby boomer earns $313.70 less annually for every one-point increase in her B.M.I., while the typical male earns $161.30 less for every point.

So, another reason for me to reach my goal of achieving an "ideal" BMI of between 21 and 24.

Moreover, research has shown that employers discriminate against overweight people - probably because they do not want to be burdened with higher health insurance costs, or possibly just because they believe the obese are lazy, weak-willed or considered too unattractive to interact with customers. Reaerch by John H. Cawley, of Cornell University, found that a weight increase of 64 pounds above the average for white women was associated with 9 percent lower wages.

The obese accumulate only about half the assets of the normal-size American - for every one-point increase in BMI index, net worth dropped by $1,000. The typical female baby boomer earns $313.70 less annually for every one-point increase in her B.M.I., while the typical male earns $161.30 less for every point.

So, another reason for me to reach my goal of achieving an "ideal" BMI of between 21 and 24.

Friday, 1 December 2006

For a Fist Full of Dollars

Yes, I'm officially a tightwad.

My eldest son (6) was excited that I've noticed and picked up a 5c coin twice this week (the money goes into his money box). I'm a bit worried though, that he wasn't impressed that it was "only" a 5c coin, and that it would take 20 of them to make $1. Stopping to pick up small change must run in our family though, because he told me that his Grandpa and done the same thing the other day.

And then, yesterday, I spent an hour in the city walking around two of the large uni campuses sticking up notices on the student notice boards - I'd printed out some info on how to open an account with EasyStreet.com.au and get a $20 "member-get-member" bonus (if they used the referral details provided). I'll get $20 each time someone opens an account this way - I'll let you all know if anything turns up in my bank account. Anyhow, I'd gotten $20 bonus when my mom opened an account, so I know it could work (in theory).

Meanwhile I rationlise it as a brisk one hour walk which was good for my health, and provided some cheap entertainment (otherwise I'd have gone to the mall, bought some junk food and browsed the bookshops).

My eldest son (6) was excited that I've noticed and picked up a 5c coin twice this week (the money goes into his money box). I'm a bit worried though, that he wasn't impressed that it was "only" a 5c coin, and that it would take 20 of them to make $1. Stopping to pick up small change must run in our family though, because he told me that his Grandpa and done the same thing the other day.

And then, yesterday, I spent an hour in the city walking around two of the large uni campuses sticking up notices on the student notice boards - I'd printed out some info on how to open an account with EasyStreet.com.au and get a $20 "member-get-member" bonus (if they used the referral details provided). I'll get $20 each time someone opens an account this way - I'll let you all know if anything turns up in my bank account. Anyhow, I'd gotten $20 bonus when my mom opened an account, so I know it could work (in theory).

Meanwhile I rationlise it as a brisk one hour walk which was good for my health, and provided some cheap entertainment (otherwise I'd have gone to the mall, bought some junk food and browsed the bookshops).

Update: AU Stock Portfolio - 1 Dec 2006

My stock portfolio ended up 7.25% this month. $6000 of my Telstra Installment Warrant purchase has appeared in my Leveraged Equities Margin Loan account, the other $4000 worth ended up being issuer sponsored (I had expected them to be part of my Comsec Margin Loan account) - I should have looked more closely at the "personalised" offer documentation I filled in for this allocation. It doesn't really matter - I have low gearing level on my comsec account, so the extra equity isn't required. If I transferred this allotment to my Comsec account I would lose out on the 10c discount on the second payment (due in 2008) and the 1:25 "loyalty" bonus share issue. So I'll leave this allotment as issuer sponsored until after the final payment and bonus share allotment is completed.

Current holdings:

stocks

Current holdings:

Leveraged Equities Account (loan balance $155,585.68, value $287,540.31)

AAN Alinta Mergeco Ltd 295 $10.220 $3,014.90 70% $2,110.43 1%

AEO Austereo 1,405 $2.150 $3,020.75 65% $1,963.49 1%

AGK AGL Energy Limited 510 $15.500 $7,905.00 70% $5,533.50 3%

AMP AMP 720 $9.450 $6,804.00 75% $5,103.00 2%

ANN Ansell 480 $11.300 $5,424.00 70% $3,796.80 2%

ANZ ANZ Bank 1,107 $28.100 $31,106.70 75% $23,330.03 11%

BHP BHP Billiton 748 $25.930 $19,395.64 75% $14,546.73 7%

BSL Bluescope Steel 781 $8.130 $6,349.53 70% $4,444.67 2%

CASH Adelaide Bank CMT 14 $1.000 $14.94 100% $14.94 0%

CDF C/wealth Divers Fund 6,700 $1.750 $11,725.00 70% $8,207.50 4%

CHB Coca Cola Hellenic 118 $44.250 $5,221.50 65% $3,393.98 2%

DJS David Jones 2,000 $3.770 $7,540.00 65% $4,901.00 3%

FGL Foster's Group 3,751 $6.550 $24,569.05 75% $18,426.79 9%

LLC Lend Lease Corp 481 $17.300 $8,321.30 70% $5,824.91 3%

MYP Mayne Pharma Ltd 2,778 $4.120 $11,445.36 70% $8,011.75 4%

NAB National Aust Bank 309 $38.600 $11,927.40 75% $8,945.55 4%

QAN QANTAS Airways 2,175 $5.060 $11,005.50 70% $7,703.85 4%

QBE QBE Insurance 966 $25.250 $24,391.50 75% $18,293.63 8%

SGM Sims Gp Limited. 830 $19.600 $16,268.00 70% $11,387.60 6%

SUN Suncorp-Metway 850 $20.170 $17,144.50 75% $12,858.38 6%

SYB Symbion Health 2,848 $3.510 $9,996.48 70% $6,997.54 3%

TLS Telstra Corp 5,000 $3.730 $18,650.00 80% $14,920.00 6%

TLSCA Telstra (T3) 3,000 $2.300 $6,900.00 80% $5,520.00 2%

VRL Village Roadshow 1,500 $2.900 $4,350.00 60% $2,610.00 2%

WDC Westfield Group 783 $19.220 $15,049.26 75% $11,286.95 5%

Comsec Account (loan balance $94,108.28, value $191,706.31)

AGK AGL ENERGY LIMITED 240 15.560 $3,734.40 70.00 % $2,614.08

AAN ALINTA LIMITED 139 10.220 $1,420.58 70.00 % $994.41

APAR AUSTRALIAN PIPELINE TRUST 1,032 0.410 $423.12 0.00 % $0.00

APA AUSTRALIAN PIPELINE TRUST 3,612 4.160 $15,025.92 70.00 % $10,518.14

ASX AUSTRALIAN STOCK EXCHANGE 200 36.130 $7,226.00 70.00 % $5,058.20

CBA COMMONWEALTH BANK OF AUSTRALIA. 130 47.120 $6,125.60 75.00 % $4,594.20

CDF COMMONWEALTH DIVERSIFIED FUND 43,997 1.752 $77,082.74 70.00 % $53,957.92

IPEO ING PRIVATE EQUITY ACCESS OPT. 54,000 0.075 $4,050.00 0.00 % $0.00

IPE ING PRIVATE EQUITY ACCESS 8,000 0.970 $7,760.00 60.00 % $4,656.00

IFL IOOF HOLDINGS LIMITED 1,300 10.230 $13,299.00 50.00 % $6,649.50

NCM NEWCREST MINING LIMITED 300 25.670 $7,701.00 60.00 % $4,620.60

OST ONESTEEL LIMITED 2,000 4.500 $9,000.00 60.00 % $5,400.00

QBE QBE INSURANCE GROUP LIMITED 607 25.250 $15,326.75 75.00 % $11,495.06

RIO RIO TINTO LIMITED 60 74.520 $4,471.20 75.00 % $3,353.40

THG THAKRAL HOLDINGS GROUP 4,000 0.910 $3,640.00 50.00 % $1,820.00

WBC WESTPAC BANKING CORPORATION 300 23.900 $7,170.00 75.00 % $5,377.50

WPL WOODSIDE PETROLEUM LIMITED 220 37.500 $8,250.00 75.00 % $6,187.50

Leveraged Equities Account (loan balance $155,585.68, value $287,540.31)

AAN Alinta Mergeco Ltd 295 $10.220 $3,014.90 70% $2,110.43 1%

AEO Austereo 1,405 $2.150 $3,020.75 65% $1,963.49 1%

AGK AGL Energy Limited 510 $15.500 $7,905.00 70% $5,533.50 3%

AMP AMP 720 $9.450 $6,804.00 75% $5,103.00 2%

ANN Ansell 480 $11.300 $5,424.00 70% $3,796.80 2%

ANZ ANZ Bank 1,107 $28.100 $31,106.70 75% $23,330.03 11%

BHP BHP Billiton 748 $25.930 $19,395.64 75% $14,546.73 7%

BSL Bluescope Steel 781 $8.130 $6,349.53 70% $4,444.67 2%

CASH Adelaide Bank CMT 14 $1.000 $14.94 100% $14.94 0%

CDF C/wealth Divers Fund 6,700 $1.750 $11,725.00 70% $8,207.50 4%

CHB Coca Cola Hellenic 118 $44.250 $5,221.50 65% $3,393.98 2%

DJS David Jones 2,000 $3.770 $7,540.00 65% $4,901.00 3%

FGL Foster's Group 3,751 $6.550 $24,569.05 75% $18,426.79 9%

LLC Lend Lease Corp 481 $17.300 $8,321.30 70% $5,824.91 3%

MYP Mayne Pharma Ltd 2,778 $4.120 $11,445.36 70% $8,011.75 4%

NAB National Aust Bank 309 $38.600 $11,927.40 75% $8,945.55 4%

QAN QANTAS Airways 2,175 $5.060 $11,005.50 70% $7,703.85 4%

QBE QBE Insurance 966 $25.250 $24,391.50 75% $18,293.63 8%

SGM Sims Gp Limited. 830 $19.600 $16,268.00 70% $11,387.60 6%

SUN Suncorp-Metway 850 $20.170 $17,144.50 75% $12,858.38 6%

SYB Symbion Health 2,848 $3.510 $9,996.48 70% $6,997.54 3%

TLS Telstra Corp 5,000 $3.730 $18,650.00 80% $14,920.00 6%

TLSCA Telstra (T3) 3,000 $2.300 $6,900.00 80% $5,520.00 2%

VRL Village Roadshow 1,500 $2.900 $4,350.00 60% $2,610.00 2%

WDC Westfield Group 783 $19.220 $15,049.26 75% $11,286.95 5%

Comsec Account (loan balance $94,108.28, value $191,706.31)

AGK AGL ENERGY LIMITED 240 15.560 $3,734.40 70.00 % $2,614.08

AAN ALINTA LIMITED 139 10.220 $1,420.58 70.00 % $994.41

APAR AUSTRALIAN PIPELINE TRUST 1,032 0.410 $423.12 0.00 % $0.00

APA AUSTRALIAN PIPELINE TRUST 3,612 4.160 $15,025.92 70.00 % $10,518.14

ASX AUSTRALIAN STOCK EXCHANGE 200 36.130 $7,226.00 70.00 % $5,058.20

CBA COMMONWEALTH BANK OF AUSTRALIA. 130 47.120 $6,125.60 75.00 % $4,594.20

CDF COMMONWEALTH DIVERSIFIED FUND 43,997 1.752 $77,082.74 70.00 % $53,957.92

IPEO ING PRIVATE EQUITY ACCESS OPT. 54,000 0.075 $4,050.00 0.00 % $0.00

IPE ING PRIVATE EQUITY ACCESS 8,000 0.970 $7,760.00 60.00 % $4,656.00

IFL IOOF HOLDINGS LIMITED 1,300 10.230 $13,299.00 50.00 % $6,649.50

NCM NEWCREST MINING LIMITED 300 25.670 $7,701.00 60.00 % $4,620.60

OST ONESTEEL LIMITED 2,000 4.500 $9,000.00 60.00 % $5,400.00

QBE QBE INSURANCE GROUP LIMITED 607 25.250 $15,326.75 75.00 % $11,495.06

RIO RIO TINTO LIMITED 60 74.520 $4,471.20 75.00 % $3,353.40

THG THAKRAL HOLDINGS GROUP 4,000 0.910 $3,640.00 50.00 % $1,820.00

WBC WESTPAC BANKING CORPORATION 300 23.900 $7,170.00 75.00 % $5,377.50

WPL WOODSIDE PETROLEUM LIMITED 220 37.500 $8,250.00 75.00 % $6,187.50

stocks

APA Renounceable Rights Issue is Bad for the Small Investor

I received a thick wad of information in the post yesterday about a 2 for 7 renounceable rights issue from Australian Pipeline Trust. The rights are to purchase additional APA shares at $3.75 (a discount of around 15% to the current share price). Sounds OK, doesn't it? Well, yes, for most investors it's OK, even if not the windfall some may think. (As the new shares issued at this reduced price tend to make the share price drop for your current holding, so it all generally averages out - the only real benefit is that the company is getting funding at a better rate than it could get elsewhere).

However, while I'm OK with having to fork out around $3,800 to take up the rights issue (in fact I sent it on to my margin lender today, so the amount will simply be added on to my margin loan balance, so it won't affect my cashflow), some smaller shareholders may find themselves losing out. If they do not take up the offer, then the rights expire with no value, and the underwriter will, in effect, purchase the relevant number of shares that would have been issued. In this case the small shareholder will get no immediate benefit from the rights issue, and will suffer from having the share holding interest in the company diluted by the new shares issued to other shareholders and the underwriter.

Theoretically any shareholders who don't want to take up the rights issue can sell their rights on the market and get a benefit that way. But there are a couple of obstacles facing the smaller shareholders:

* the trading of the rights ends on Monday, and the offer document only arrived in the post yesterday. Any small shareholders who are unsure what to do, or don't currently have a relationship with a broker, doesn't have much time to take action.

* A small shareholder with, for example, $1000 worth of APA shares (around 235 shares) would have received rights to purchase an additional 67 shares at $3.75 - a cost of $251.25. But, if they didn't want to buy more APA shares, then they'd have rights worth AT MOST $33.50. Even at discount brokerage rates it would be hard to sell such a parcel for more than the brokerage costs!

APA has chosen to restrict the rights offer to Australian and New Zealand shareholders, as it would be too expensive to print relevant documentation for other foreign shareholders, given the different laws and regulations applicable to such an offer in other countries. For FOREIGN shareholders, APA will sell the relevant number of rights on market, and send the proceeds to such foreign shareholders.

If APA had the best interests of small shareholders in mind, they would have used the money obtained from the underwriter for all expired rights to make similar payments to any Australian or New Zealand share holders who didn't sell or accept the rights offer.

However, while I'm OK with having to fork out around $3,800 to take up the rights issue (in fact I sent it on to my margin lender today, so the amount will simply be added on to my margin loan balance, so it won't affect my cashflow), some smaller shareholders may find themselves losing out. If they do not take up the offer, then the rights expire with no value, and the underwriter will, in effect, purchase the relevant number of shares that would have been issued. In this case the small shareholder will get no immediate benefit from the rights issue, and will suffer from having the share holding interest in the company diluted by the new shares issued to other shareholders and the underwriter.

Theoretically any shareholders who don't want to take up the rights issue can sell their rights on the market and get a benefit that way. But there are a couple of obstacles facing the smaller shareholders:

* the trading of the rights ends on Monday, and the offer document only arrived in the post yesterday. Any small shareholders who are unsure what to do, or don't currently have a relationship with a broker, doesn't have much time to take action.

* A small shareholder with, for example, $1000 worth of APA shares (around 235 shares) would have received rights to purchase an additional 67 shares at $3.75 - a cost of $251.25. But, if they didn't want to buy more APA shares, then they'd have rights worth AT MOST $33.50. Even at discount brokerage rates it would be hard to sell such a parcel for more than the brokerage costs!

APA has chosen to restrict the rights offer to Australian and New Zealand shareholders, as it would be too expensive to print relevant documentation for other foreign shareholders, given the different laws and regulations applicable to such an offer in other countries. For FOREIGN shareholders, APA will sell the relevant number of rights on market, and send the proceeds to such foreign shareholders.

If APA had the best interests of small shareholders in mind, they would have used the money obtained from the underwriter for all expired rights to make similar payments to any Australian or New Zealand share holders who didn't sell or accept the rights offer.

Saving money when buying real estate

Although the overall returns from real estate are similar to that of stocks in the long term, there are some aspects that make real estate less attractive to some investors:

* its price isn't known daily like the quoted stocks, only when a sale is made. Between sales estimates based on similar sales in the area have to suffice

* it can only be bought and sold in large "chunks" - as they say, you can't sell off one bedroom of a house if you need some cash

* there are relatively high transaction costs compared to buying and selling shares - compare typical stock brokerage fees of less than 1% to real estate agents fees of over 5% in many cases.

At long least competition appears to be starting to reduce fees somewhat. For example AlCan Realty Partners, LLC is offering a 1.5% cash rebate at closing when purchasing Dallas Real Estate. Their website currently lists 50,567 properties. Hopefully similar rebate schemes will become common in all areas, and competition will force other agents to reduce their commissions.

PayPerPost

* its price isn't known daily like the quoted stocks, only when a sale is made. Between sales estimates based on similar sales in the area have to suffice

* it can only be bought and sold in large "chunks" - as they say, you can't sell off one bedroom of a house if you need some cash

* there are relatively high transaction costs compared to buying and selling shares - compare typical stock brokerage fees of less than 1% to real estate agents fees of over 5% in many cases.

At long least competition appears to be starting to reduce fees somewhat. For example AlCan Realty Partners, LLC is offering a 1.5% cash rebate at closing when purchasing Dallas Real Estate. Their website currently lists 50,567 properties. Hopefully similar rebate schemes will become common in all areas, and competition will force other agents to reduce their commissions.

PayPerPost

A Word a Day: "Dividend Yield"

A numerical measure that relates dividends to the current share price and puts ordinary dividends on a relative (percentage) rather than an absolute (dollar) basis. This makes it easier to compare the yields of different stocks.

The average dividend yield of the whole market (or a particular segment) is often compared to the typical (long-run) average dividend yield in order to determine if the market (or segment) is over-priced, fair value, or under-priced.

This is only an approximation however, because the dividend yield calculation is based on historic dividends and the current share price to try to predict the future. Some analysts will modify this measure to make use of estimated or "prospective" earnings to decide if current prices are fair value. Of course this is only as accurate as your estimation of prospective earnings.

The average dividend yield of the whole market (or a particular segment) is often compared to the typical (long-run) average dividend yield in order to determine if the market (or segment) is over-priced, fair value, or under-priced.

This is only an approximation however, because the dividend yield calculation is based on historic dividends and the current share price to try to predict the future. Some analysts will modify this measure to make use of estimated or "prospective" earnings to decide if current prices are fair value. Of course this is only as accurate as your estimation of prospective earnings.

Indebted and desperate