The problem is that a large proportion of these borrowers really can't afford to service the loan, and are a risk of defaulting on loan payments if anything goes wrong.

Banks have been increasingly lending to such "high risk" borrowers in order to maintain their market share and profitability. Despite a couple of periods where stock analysts were advising that bank stocks had peaked, with their profit margins starting to be squeezed, banks have been a consistently good investment over the past decade:

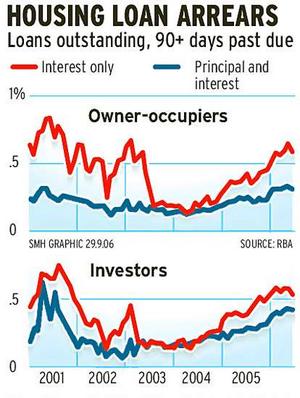

Now, however, I'm thinking seriously about reducing my exposure to bank stocks. The trend in home loan defaults is a bit worrying, and may impact bank profits in the medium term:

Then again, realising capital gains is always a pain in the tax, especially this financial year when my wife is on maternity leave - any extra taxable income could impact her chance of getting any family tax benefit, which means the effective tax rate of realising capital gains this year is prohibitive. Also, as a "long term" investor, trying to dabble in market timing is generally a bad idea.

eenie, meenie, miny, moe...

Disclaimer: I am NOT giving financial advice. Do NOT really on any opinion expressed in this blog when making decisions about YOUR money. Do your own research, seek professional advice as needed. I currently own shares in the following banks: ANZ, CBA, NAB, SUN and WBC.

No comments:

Post a Comment