There have been a many discussions on the pf blogs about how one calculates new worth - should we or shouldn't we include our cars, our stereo, our collection of yo-yos (not so silly: see this recent article about the value of old yo-yos) in our estimation of new worth? I came across some useful information about this which is worth sharing [ref: Annual Review of Sociology: Vol 26, p.502]

* Wealth is commonly identified with net worth and assessed as the difference between the total value of family assets and the amount of debt.

* There are various categories of household assets, with different features, so it is important to distinguish between them. Depending on which assets you include, net worth can be defined [Wolff, 1995] as:

Marketable Wealth - net worth excluding consumer durables such as automobiles, television and household appliances. The rationale being that these have less resale value than their consumption service to the family, so would usually not be sold to raise funds. This exclusion tends to impact poorer households to a greater extent, as consumer durables, especially cars, are the main "asset" of such families.

Financial Wealth - marketable Wealth minus equity in owner-occupied housing. As you need to live somewhere, it is often difficult to convert it into cash in the short term. In places such as Australia where superannuation is "preserved" (unable to be used for any purpose) until retirement age, it may be worth also excluding the value of your retirement account. I do both - my Net Worth tracked with NetWorthIQ is by "Marketable Wealth", and in my daily Net Worth spreadsheet updates I also have a column of Net Worth minus home and super.

Augmented Wealth - this includes some items not normally included in net worth estimates. Specifically, a discounted present value is calculated for any pension and social security retirement benefit.

BTW - while reading this paper I also came upon the following factoid:

"According to the Lampman-Smith_schwartz time series [Committee on Ways and Means 1992, p.1564], the richest 1% of the US population owned 36% of household net worth in 1929, but by 1982 the figure had dropped to 20%" although the data since 1982 is less clear - the decline may have continued or reversed somewhat.

ie. The Rich are getting POORER! This is probably why social commentators have recently started lamenting the income gap between CEO salaries and the average wage, rather than the traditional cry that the wealth gap between rich and poor is widening (although they still raise this topic on occasion - they simply refer the difference between rich and poor increasing in dollar terms, rather than in % terms, which wouldn't support their agenda.

Wednesday, 29 November 2006

Student Loans

It's generally accepted that, provided you choose the right school and qualification, higher education can be a good long-term investment. The problem is, it can require a substantial amount of money at a time when you are not earning much, if anything, and you probably do not have an accumulation of savings to draw upon. For this reason student loans are often required, and you may also be interested in a Private Student Loan from NextStudent.com.

Undergraduates and graduates can borrow annually up to the full cost of expenses (less any financial aid received) or $40,000 (whichever is the lesser amount) from NextStudent.com. Even if you're not shopping around for a private student loan, their website also has some useful information on:

* Student Loan Advice

* Financial Aid Tutorial

* Scholarship Search

* Compare Loans

* Tools and Resources

* Directory of Schools

sponsored

Undergraduates and graduates can borrow annually up to the full cost of expenses (less any financial aid received) or $40,000 (whichever is the lesser amount) from NextStudent.com. Even if you're not shopping around for a private student loan, their website also has some useful information on:

* Student Loan Advice

* Financial Aid Tutorial

* Scholarship Search

* Compare Loans

* Tools and Resources

* Directory of Schools

sponsored

Tuesday, 28 November 2006

Coins or Paper?

There have been a few posts recently about the new US dollar coins that will be coming out. They probably won't replace paper for a while as the paper notes will remain in circulation. As we've had polymer notes and $1 and $2 coins for many years in Oz, I was wondering if the "paper for dollars" hang-up is specific to the US. So I had a quick search around to find out what paper/coin currency mix other developed countries are using:

amounts marked with an * are not in common use

amounts marked with a^ are mainly in use as notes

% - Australian also produces a range of silver and gold "legal tender" coins in deominataions such as $3, $10, $100, $200 - but these are issued in proof or uncirculated condition for coin collectors, not general circulation.

I believe that larger US notes (over $100) are similar - they exist (I think they were initially intended for bank transfers of funds) but are not in general circulation.

It certainly appears that the USA has the smallest denomination folding money still in use.

Country Coins Both Notes

Australia% 5c,10c,20c,50c,$1,$2 $5^ $10,$20,$50,$100

United Kingdon 1p,2p,5p,10p,20p,50p,£1,£2 - £5,£10,£20,£50*

United States 1c,5c,10c,25c,50c $1^ $1,$2,$5,$10,$20,$50,$100

Eurozone 1c,2c,5c,10c,20c,50c,€1,€2 - €5,€10,€20,€50,€100,€200,€500

Japan ¥1,¥5,¥10,¥50,¥100,¥500 ¥1000,¥2000,¥5000,¥10000

amounts marked with an * are not in common use

amounts marked with a^ are mainly in use as notes

% - Australian also produces a range of silver and gold "legal tender" coins in deominataions such as $3, $10, $100, $200 - but these are issued in proof or uncirculated condition for coin collectors, not general circulation.

I believe that larger US notes (over $100) are similar - they exist (I think they were initially intended for bank transfers of funds) but are not in general circulation.

It certainly appears that the USA has the smallest denomination folding money still in use.

Monday, 27 November 2006

Mortgage Fraud

If you are investing in a house for yourself or as an investment, it will probably be one of the biggest investments you make. You can help avoid being a victim of fraud when you obtain your mortgage loan by learning the ins and outs of borrowing intelligently and how to spot and avoid mortgage fraud and data abuse. PersonalHomeLoanMortgages.com has articles about

* The Truth in Lending Act

* The Basics of home mortgages

* Prequalified vs Pre-approved Home Mortgages

* Home Equity Loans

* The Mortgage Refinancing Boom

* Leveraging Home Equity for Debt Consolidation

* Understanding Home Equity Loans

* Understanding Mortgage Brokers

* Reverse Mortgages

PayPerPost

* The Truth in Lending Act

* The Basics of home mortgages

* Prequalified vs Pre-approved Home Mortgages

* Home Equity Loans

* The Mortgage Refinancing Boom

* Leveraging Home Equity for Debt Consolidation

* Understanding Home Equity Loans

* Understanding Mortgage Brokers

* Reverse Mortgages

PayPerPost

A Word a Day: "Beta"

A measure of non-diversifiable, or market, risk that indicates how the price of a security reacts to market forces.

Sunday, 26 November 2006

The Four Deadly Sins of Personal Finance

An very interesting article in the NYT reminded me, again, of the four deadly sins of personal finance:

1. Greed - "just a little bit more" can easily become "too much", whether it be chasing higher investment returns, pinching pennies, or getting "top dollar" when selling or "a bargain" when making a purchase. Remember the old adage that if it "looks too good to be true it probably is". When looking for "overlooked" investment opportunities it's also worth bearing in mind that there are several billion other human beings out there, millions of whom are also looking for the "overlooked".

2. Sloth - most people apparently spend more time planning the annual holiday than they do on planning their finances. Aside from generally financial planning, you also have to put in sufficient effort to analyse each potential investment on its merits. Buy things purely on the say-so of a friend or relative and you will have no-one to blame but yourself if things don't work out.

3. Trust - yes, BLIND trust can be a very bad thing. As they say in auditor-land "trust but verify" - don't take anyone's word for something that you could verify. And if there is nothing to back-up someone's verbal assurance, flag this mentally as having an "unknown amount of risk"

4. Envy - just because every one else seems to be making a fortune investing by in "X" doesn't mean you should try it. It doesn't even mean that they are actually making any money from "X". Not only can appearances be deceiving, I'd say that they usually are deceiving.

personal finance, investing

1. Greed - "just a little bit more" can easily become "too much", whether it be chasing higher investment returns, pinching pennies, or getting "top dollar" when selling or "a bargain" when making a purchase. Remember the old adage that if it "looks too good to be true it probably is". When looking for "overlooked" investment opportunities it's also worth bearing in mind that there are several billion other human beings out there, millions of whom are also looking for the "overlooked".

2. Sloth - most people apparently spend more time planning the annual holiday than they do on planning their finances. Aside from generally financial planning, you also have to put in sufficient effort to analyse each potential investment on its merits. Buy things purely on the say-so of a friend or relative and you will have no-one to blame but yourself if things don't work out.

3. Trust - yes, BLIND trust can be a very bad thing. As they say in auditor-land "trust but verify" - don't take anyone's word for something that you could verify. And if there is nothing to back-up someone's verbal assurance, flag this mentally as having an "unknown amount of risk"

4. Envy - just because every one else seems to be making a fortune investing by in "X" doesn't mean you should try it. It doesn't even mean that they are actually making any money from "X". Not only can appearances be deceiving, I'd say that they usually are deceiving.

personal finance, investing

Saturday, 25 November 2006

All I want for Christmas

Yet another Christmas approaches with the usual breaking of the agreement that the adults won't bother exchanging gifts. I've previously tried insisting that I really didn't want anything for Christmas from my parents (aside from watching DS1 opening his presents from his grandparents after the traditional huge family Christmas Eve dinner), but I always ended up getting "something" - usually an electronic knick-knack that I don't really want which then just clutters up the house for several years until it gets thrown out.

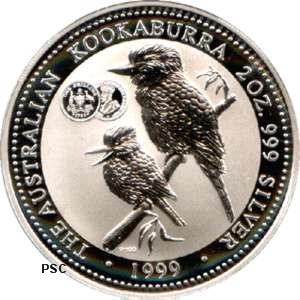

So, this year I decided I may as well prepare for the inevitable and ask for something that has an intrinsic value, I'll actually like, and won't take up too much space - silver coins. I already have a coin collection, so a few additions each year won't create any new storage problems. My mum had no idea how to order what I wanted, so I ordered them online and mum will pay me back (apparently adults don't need a Christmas present to be a surprise, but do need a wrapped up present to exchange). As my birthday is a couple of weeks before Christmas I ordered two items - a 2005 1oz costing $30 for my birthday present and a 1999 2 oz 99.9% Silver Kookaburra (Perth Mint Privy Mark, 1933 Shilling) coin costing $75 for Christmas.

The silver content of these coins is worth about 50% of the cost, and the same 2oz proof coin is listed elsewhere and on ebay for $120, so I think it's a good buy at $75.

investing, money, saving

So, this year I decided I may as well prepare for the inevitable and ask for something that has an intrinsic value, I'll actually like, and won't take up too much space - silver coins. I already have a coin collection, so a few additions each year won't create any new storage problems. My mum had no idea how to order what I wanted, so I ordered them online and mum will pay me back (apparently adults don't need a Christmas present to be a surprise, but do need a wrapped up present to exchange). As my birthday is a couple of weeks before Christmas I ordered two items - a 2005 1oz costing $30 for my birthday present and a 1999 2 oz 99.9% Silver Kookaburra (Perth Mint Privy Mark, 1933 Shilling) coin costing $75 for Christmas.

The silver content of these coins is worth about 50% of the cost, and the same 2oz proof coin is listed elsewhere and on ebay for $120, so I think it's a good buy at $75.

investing, money, saving

Payday loans

Payday loans are short-term advances that are due on your next payday, unless your next payday is 4 or less days away from your loan date - in that case your loan will be due on your second payday. Hence, the maximum loan term is 16 days. Payday loans are available from nationalpayday.com and others. Payday loans short-term advances intended to be paid off quickly - so they're really only suitable for SHORT TERM cash flow requirements. The loans involve a standard fee of $25 per $100 loaned, so the effective APR values are not really relevant - you're getting 75% of your pay in exchange for receiving it in advance, and have to pay off the full amount when you get your pay check. Thus you should really only use such loans in an emergency, hopefully in order to avoid pay even higher fees elsewhere.

For example, you might need an emergency cash advance via a payday loan to avoid eviction, avoid hefty late payment penalties and higher interest rates on your CC debt, or other emergency cash requirements. Sometimes it can be more expensive to source funds for apparently cheaper sources - for example, although the APR rate for a personal loan or bank overdraft facility may be lower, there may be an establishment fee that ends up higher than the $25 per $100 charged by nationalpayday.com. There can also be costs associated with setting up a bank overdraft facility that is seldom used, either a monthly admin fee or a charge based on the overdraft limit, even when not in use. For these reasons, it can sometimes be more economical to make use of a payday loan for emergency cash requirements, even if you were able to source funds from another source. One other potential benefit of a payday loan from nationalpayday.com is that they don't make a credit check when you apply - so this might mean that your credit rating doesn't suffer from a hard credit enquiry.

sponsored

For example, you might need an emergency cash advance via a payday loan to avoid eviction, avoid hefty late payment penalties and higher interest rates on your CC debt, or other emergency cash requirements. Sometimes it can be more expensive to source funds for apparently cheaper sources - for example, although the APR rate for a personal loan or bank overdraft facility may be lower, there may be an establishment fee that ends up higher than the $25 per $100 charged by nationalpayday.com. There can also be costs associated with setting up a bank overdraft facility that is seldom used, either a monthly admin fee or a charge based on the overdraft limit, even when not in use. For these reasons, it can sometimes be more economical to make use of a payday loan for emergency cash requirements, even if you were able to source funds from another source. One other potential benefit of a payday loan from nationalpayday.com is that they don't make a credit check when you apply - so this might mean that your credit rating doesn't suffer from a hard credit enquiry.

sponsored

A Word a Day: "Market Order"

An order to buy or sell securities at the best price available when the order is placed.

Friday, 24 November 2006

How much can a kid earn?

Well, aside from child actors - I mean how much can your normal, average kid earn? I've no idea really, but it's been interesting to see how much my son managed to earn doing a couple of casual jobs. DS1 earned about $80 a week doing a paper round for almost two years - he enjoyed the morning walks with his dad and stuffing the folded papers into the letter boxes. As it took 2 hours to deliver the papers, five days a week, this works out at $8 an hour for him - a pretty good hourly rate for a primary school kid. But, this isn't counting dad's time spent supervising and lifting newspaper bundles, or the cost of driving to and from the paper route.

More recently he'd started learning the recorder at school, and enjoyed performing at the school concerts, so I got him a busking licence from the city council. When he was in the city for his Saturday morning music lessons we'd take the opportunity to let him busk for a short while. At his age he gets lots of interest from the passing tourists, especially when he's wearing his medieval jester's cap. He has sometimes earned a surprising amount in a very short time - the exact amount depending mainly on the location chosen. In the main city park there was a lot of passing trade, but very few people stopped to listen. The average amount contributed was also small - around 10c-50c per person from this audience. The return was much higher outside the public art gallery - the pedestrian traffic flow was less, but the audience was more appreciative, included lots more tourists, and the amount contributed was typically higher - some contributions were $1 or more.

My son enjoyed busking for short periods - after 10 minutes he'd lose interest and need a break (a quick tour through the art gallery was always fun). Then, after a second 5-10 minute session he'd knock off for the day. One time he got carried away and kept playing for 45 minutes! He quite enjoyed earning the money, counting it afterwards, and depositing it into his savings account. Now that he's finished his music lessons in town he probably won't get a chance to do any more busking unless we're in the city anyway to visit a museum, go shopping or take in a movie.

He's been busy learning Christmas carols in his recorder class, so if we go into the city to visit the Maritime museum before Christmas he may get another chance to busk this year.

So far his earnings from busking are:

15 mins $ 2.35 (park)

15 mins $ 6.30

20 mins $ 6.80 (park)

20 mins $12.15

30 mins $10.65

30 mins $19.85

45 mins $49.65

20 mins $10.95

All up, $118.70 for 3.15 hours work = $37.68 an hour!

His annual busking licence cost me $41 and expires next May. (For Sydney City busking details see this) I don't think I'll renew the licence next year as we probably won't be in the city often enough to make it worthwhile (I pay for the licence so it doesn't cut into his earnings, but I'd like him to make more than the licence cost me, otherwise I may as well just increase his allowance and he can spend the time practicing at home). Unfortunately our local council only allows busking in very restricted areas and the licence fee is exhorbitant, so it's really the City or nowhere.

More recently he'd started learning the recorder at school, and enjoyed performing at the school concerts, so I got him a busking licence from the city council. When he was in the city for his Saturday morning music lessons we'd take the opportunity to let him busk for a short while. At his age he gets lots of interest from the passing tourists, especially when he's wearing his medieval jester's cap. He has sometimes earned a surprising amount in a very short time - the exact amount depending mainly on the location chosen. In the main city park there was a lot of passing trade, but very few people stopped to listen. The average amount contributed was also small - around 10c-50c per person from this audience. The return was much higher outside the public art gallery - the pedestrian traffic flow was less, but the audience was more appreciative, included lots more tourists, and the amount contributed was typically higher - some contributions were $1 or more.

My son enjoyed busking for short periods - after 10 minutes he'd lose interest and need a break (a quick tour through the art gallery was always fun). Then, after a second 5-10 minute session he'd knock off for the day. One time he got carried away and kept playing for 45 minutes! He quite enjoyed earning the money, counting it afterwards, and depositing it into his savings account. Now that he's finished his music lessons in town he probably won't get a chance to do any more busking unless we're in the city anyway to visit a museum, go shopping or take in a movie.

He's been busy learning Christmas carols in his recorder class, so if we go into the city to visit the Maritime museum before Christmas he may get another chance to busk this year.

So far his earnings from busking are:

15 mins $ 2.35 (park)

15 mins $ 6.30

20 mins $ 6.80 (park)

20 mins $12.15

30 mins $10.65

30 mins $19.85

45 mins $49.65

20 mins $10.95

All up, $118.70 for 3.15 hours work = $37.68 an hour!

His annual busking licence cost me $41 and expires next May. (For Sydney City busking details see this) I don't think I'll renew the licence next year as we probably won't be in the city often enough to make it worthwhile (I pay for the licence so it doesn't cut into his earnings, but I'd like him to make more than the licence cost me, otherwise I may as well just increase his allowance and he can spend the time practicing at home). Unfortunately our local council only allows busking in very restricted areas and the licence fee is exhorbitant, so it's really the City or nowhere.

A Word a Day: "Risk-return tradeoff"

The relationship (theoretical) between risk and return, in which investments with more risk should provide higher returns, and vice versa.

Xmas Gift Idea: Microscope for the kids

I always loved science as a kid, and one of my favourite toys (aside from my Tasco telescope) was my microscope kit. The good thing about microscopes is that they can be used anytime, they're educational, and you can find endless things to study around the house and in the garden. Later on, its a good tool for studying practical biology.

www.Microscopes.com is a brand new site from the best optical dealer www.OpticsPlanet.com. It has microscopes, accessories and gift packages at huge discounts up to 65% OFF & Free UPS on orders over $29.

For children high powered microscopes are most popular as the kids can use them to see "invisible" things like blood cells, amoebas and bacteria. As well as all the tiny critters living in a drop of pond water. Do not buy a plastic "toy" microscope, as a poor quality microscope is totally useless, so you're just throwing your money away and will disppoint the child (same goes for telescopes with poor optics and cheap, flimsy mounts). Purchase a model with a built in light source. Models with mirrors are rarely sold today. There are no manufacturers of microscopes in the US - the best "economy" models are made in China. There are some very good products from China, but also some poor quality instruments, so be careful what you buy. A good microscope can be used all through to University and beyond (my parents are in their 70s and still use a simple microscope to check for parasites on the grass at their alpaca farm).

PayPerPost

www.Microscopes.com is a brand new site from the best optical dealer www.OpticsPlanet.com. It has microscopes, accessories and gift packages at huge discounts up to 65% OFF & Free UPS on orders over $29.

For children high powered microscopes are most popular as the kids can use them to see "invisible" things like blood cells, amoebas and bacteria. As well as all the tiny critters living in a drop of pond water. Do not buy a plastic "toy" microscope, as a poor quality microscope is totally useless, so you're just throwing your money away and will disppoint the child (same goes for telescopes with poor optics and cheap, flimsy mounts). Purchase a model with a built in light source. Models with mirrors are rarely sold today. There are no manufacturers of microscopes in the US - the best "economy" models are made in China. There are some very good products from China, but also some poor quality instruments, so be careful what you buy. A good microscope can be used all through to University and beyond (my parents are in their 70s and still use a simple microscope to check for parasites on the grass at their alpaca farm).

PayPerPost

Thursday, 23 November 2006

The Other Forbes Rich list

And now for something completely different - guess who Tops Forbes Magazine's Fictional Rich List? I'll give you a hint: Lucius Malfoy comes in at number 12... check out the who's got riches beyond your wildest dreams here.

I am Sad

My attempts to give some constructive criticism seem to have gone awry ;(

Leigh Ann was moved to write

"...your life is so tainted into thinking that everyone is bad. Maybe if you spent more time getting to know people you would make more friends and be more grateful for others and their lives" after reading my comment and post. (To be fair she may not have meant that particular bit about me - she was also talking about someone else's comments in the same post. I couldn't tell exactly which bits of her post were aimed at whom.)

I glad that in the same post she pointed out that she has "... never said a bad word about anyone and I always try to keep this blog positive.", otherwise I might have got the impression she didn't like me ;)

Wednesday, 22 November 2006

Save EnoughWealth

Help! I'm deep in debt and I don't know what to do. I've run up $14,384.34 on my VISA, Discover, Mastercard, Amex, and Diner's card and earn barely enough to pay the minimum each month! I'm sitting here in Starbuck's sipping my Cashacino and looking at the $18.50 doodad holder I just bought at Target (because I felt so depressed about my debt and went shopping to feel better) - I'll have to return it later today as I really shouldn't have bought it [I also shouldn't have accepted the new store card they offered me while I was there]. BTW you can send me cash donations via my Paypal account, details of which I've accidentally put up on my site. I'm basically a really nice person, just in a bit of financial trouble....

OK - that's a load of BS. It's just that I get irritated by the SaveKaryn and SaveLeighAnne's of the world - those bloggers that have run up large *personal* debts, get help from many generous people, and basically use OPM to pay off their debts.

Now, I don't have anything against Karyn or LeighAnne wanting to pay off their debts, I don't resent them getting some help, and I certainly won't criticise anyone for being generous and donating cash to such folk to help them out. BUT - I worry that this is a very a bad example of how to "solve" your CC debt problem. And I really start to worry when I read that "I am going to start helping other's with their finances as soon as I can"!

Update: For some reason this post gets a lots of hits, so if anyone came here thinking they were going to be asked to donate money, here are some good causes (I have no association with any of them):

https://www.teamseti.org/

http://astronomerswithoutborders.org/about-us/become-a-donor.html

http://www.womancareglobal.org/

OK - that's a load of BS. It's just that I get irritated by the SaveKaryn and SaveLeighAnne's of the world - those bloggers that have run up large *personal* debts, get help from many generous people, and basically use OPM to pay off their debts.

Now, I don't have anything against Karyn or LeighAnne wanting to pay off their debts, I don't resent them getting some help, and I certainly won't criticise anyone for being generous and donating cash to such folk to help them out. BUT - I worry that this is a very a bad example of how to "solve" your CC debt problem. And I really start to worry when I read that "I am going to start helping other's with their finances as soon as I can"!

Update: For some reason this post gets a lots of hits, so if anyone came here thinking they were going to be asked to donate money, here are some good causes (I have no association with any of them):

https://www.teamseti.org/

http://astronomerswithoutborders.org/about-us/become-a-donor.html

http://www.womancareglobal.org/

A Word a Day: "Tax Risk"

The risk that governments will make unfavourable changes to tax laws, reducing after-tax returns and market prices for certain investments.

Tuesday, 21 November 2006

Carni-Festivals I contributed to This Week

What's better than pfblogs.org? Why, the Carnivals and Festivals each week - get all the best posts and none of rest! Enjoy these two already up this week:

20 NOV: Festival of Stocks #11 included my US Shares - “Little Book” Portfolio Update post

20 NOV: Carnival of Personal Finance #75 included my A Very Interesting FREE Home-Study Personal Finance Course post

20 NOV: Festival of Stocks #11 included my US Shares - “Little Book” Portfolio Update post

20 NOV: Carnival of Personal Finance #75 included my A Very Interesting FREE Home-Study Personal Finance Course post

Monday, 20 November 2006

Sheer Lunacy

In yet another example of "off the wall" market timing theories, academics Ilia D. Dichev and Troy D. Janes have postulated that returns in the 15 days around new moon dates are about double the returns in the 15 days around full moon dates. A similar result was reported by Lu Zheng in the paper "Are Investors Moonstruck? Lunar Phases and Stock Returns" which showed that stock returns are lower on the days around a full moon than on the days around a new moon - the magnitude of the return difference is 3% to 5% per annum.

As is often the case in such academic studies, there is little likelihood of creating a profitable active trading strategy out of this information due to the cost of trading 13 times a year compared to the magnitude of expected outperformance (3-5% pa). However, it may be worth bearing the lunar calendar in mind when you are thinking about buying or selling shares in your portfolio, provided that there is no urgency in completing the trade. If you are routinely adding to your portfolio in the week immediately before or after the full moon, and selling within a week of the new moon adds 3-5% to your overall returns (pa?) it could be a worthwhile strategy.

The article in the NYT shows the lunar cycle effect for various markets around the world:

investing

As is often the case in such academic studies, there is little likelihood of creating a profitable active trading strategy out of this information due to the cost of trading 13 times a year compared to the magnitude of expected outperformance (3-5% pa). However, it may be worth bearing the lunar calendar in mind when you are thinking about buying or selling shares in your portfolio, provided that there is no urgency in completing the trade. If you are routinely adding to your portfolio in the week immediately before or after the full moon, and selling within a week of the new moon adds 3-5% to your overall returns (pa?) it could be a worthwhile strategy.

The article in the NYT shows the lunar cycle effect for various markets around the world:

investing

A Word a Day: "Pyramiding"

The process of using unrealised gains to partly or fully finance the purchase of additioal securities using a margin loan.

Sunday, 19 November 2006

Anyone want $5?

I redeemed some of my MyPoints points for a $10 Webcertificates.com "giftcard" - they've emailed me the ID code and once its activated it will work like a debit card for making $10 worth of online purchases...

Only problem is that the webcertificates.com website only allows US residents to activate their giftcards (the server checks the IP address being used to connect to their activation page, and I can't get round this, even using an anonymous proxy server). So, I can send the $10 gift card details to anyone in the US who'd like to activate and use it, if you'll deposit half the value ($5) into my Paypal account (once you've got your $10 benefit).

Only problem is that the webcertificates.com website only allows US residents to activate their giftcards (the server checks the IP address being used to connect to their activation page, and I can't get round this, even using an anonymous proxy server). So, I can send the $10 gift card details to anyone in the US who'd like to activate and use it, if you'll deposit half the value ($5) into my Paypal account (once you've got your $10 benefit).

Early "Retirement"?

I'm currently enjoying my work and not too stressed out, but I can see a time in 2-3 years when I'll have been working for the same company for ten years, and with my 8 weeks "long service leave" then becoming fully vested, I could consider making another career change.

My first career, straight out of uni, was as a research scientist working on minerals processing equipment (with a bit of computer modelling and computer systems admin thrown in). This made good use of my first degree (in Applied Chem) but I actually found the programming of more interest than the chemistry (although playing around with the analytical equipment was a fun way to make a living).

After ten years my first employer laid off a large portion of the research staff in a cost-cutting drive, so I took the chance to change career into the "real world" of a private business-services company, and make use of my GradDip in Industrial Math & Computing. After taking an initial pay cut to get my foot in the door, I soon was earning more than in my old job, and had opportunity to progress up the "management ladder". But after 8 years I'm thinking of what I want to do for the next 20 years or so.

I'm currently half-way through a Masters in IT by distance ed, and I've just been accepted into a Post-Grad Diploma of Secondary Education course for next year. The plan is to finish of the MIT and the GradDipEd in the next couple of years, and then get put on the waiting list for a High School science teaching position. If I nominate only schools in the area we live (Sydney Northern Beaches) the waiting time for a position will be quite long (although they seem a bit short on Science teachers), so I probably wouldn't get a position immediately.

The plan is to accept a suitable teaching position (which will mean a pay cut of 50% or so), and treat the new job as a sort of "early retirement". The change of career should make the job interesting (at least for a decade or so), and the daily hours and amount of annual leave entitlement should make the hourly rate similar to what I currently earn - sort of like changing to a part-time job ;)

I'm sure any teacher's out there will say that teaching is anything but a part-time job, but, at least on paper, it looks like a good idea.

What do you think?

My first career, straight out of uni, was as a research scientist working on minerals processing equipment (with a bit of computer modelling and computer systems admin thrown in). This made good use of my first degree (in Applied Chem) but I actually found the programming of more interest than the chemistry (although playing around with the analytical equipment was a fun way to make a living).

After ten years my first employer laid off a large portion of the research staff in a cost-cutting drive, so I took the chance to change career into the "real world" of a private business-services company, and make use of my GradDip in Industrial Math & Computing. After taking an initial pay cut to get my foot in the door, I soon was earning more than in my old job, and had opportunity to progress up the "management ladder". But after 8 years I'm thinking of what I want to do for the next 20 years or so.

I'm currently half-way through a Masters in IT by distance ed, and I've just been accepted into a Post-Grad Diploma of Secondary Education course for next year. The plan is to finish of the MIT and the GradDipEd in the next couple of years, and then get put on the waiting list for a High School science teaching position. If I nominate only schools in the area we live (Sydney Northern Beaches) the waiting time for a position will be quite long (although they seem a bit short on Science teachers), so I probably wouldn't get a position immediately.

The plan is to accept a suitable teaching position (which will mean a pay cut of 50% or so), and treat the new job as a sort of "early retirement". The change of career should make the job interesting (at least for a decade or so), and the daily hours and amount of annual leave entitlement should make the hourly rate similar to what I currently earn - sort of like changing to a part-time job ;)

I'm sure any teacher's out there will say that teaching is anything but a part-time job, but, at least on paper, it looks like a good idea.

What do you think?

The Rich get Richer and the Super-Rich get envied

A recent study by the Center on Budget and Policy Priorities in Washington reported that while the percentage change in average real household income between 1990 and 2004 was an increase of 57% for the top 1 percent of American taxpaying households (with a annual income of $940,000 in 2004), it was 85% for the top 0.1 percent, and 112% for the top .01 percent. That is, the richest are getting richer almost twice as fast as the rich.

An article in the NYT outlines how this is leading to resentment by the bigger and poorer group, the "lower uppers" which consists largely of professionals (doctors, lawyers, management consultants, most Wall Street execs), for hedge fund managers and some astronomically paid C.E.O.’s who are seen to be undeserving of the huge amounts they receive.

It's difficult to feel sorry for the "merely rich" though - in the same time period the percentage change in average real household income was an increase of 2 percent for the bottom 90 percent of American households.

money, wealth

An article in the NYT outlines how this is leading to resentment by the bigger and poorer group, the "lower uppers" which consists largely of professionals (doctors, lawyers, management consultants, most Wall Street execs), for hedge fund managers and some astronomically paid C.E.O.’s who are seen to be undeserving of the huge amounts they receive.

It's difficult to feel sorry for the "merely rich" though - in the same time period the percentage change in average real household income was an increase of 2 percent for the bottom 90 percent of American households.

money, wealth

Saturday, 18 November 2006

Frugal living: Bottled Water

I take bottled drinking water to work - although Sydney tap water is of good quality, I don't want to drink the tap water in my office because the building is an old converted factory building, and I'm not sure how good the pipes are. Having bought a couple of bottles of drinking water I now rotate the bottles and refill them each night with chilled filtered tap water. The filtered water costs a few cents a bottle, and the quality is just as good as your typical bottled water brand by all accounts.

If you want to impress your workmates you can spend it up on the initial purchase of bottled water and have "exclusive" name brand bottles for your home made bottled water ;)

I usually also pop half a tablet of aspirin into the bottle in the morning - I happen to like the taste of aspirin, don't have any stomach problems, and the 150mg a day of aspirin might be good for my health.

saving

If you want to impress your workmates you can spend it up on the initial purchase of bottled water and have "exclusive" name brand bottles for your home made bottled water ;)

I usually also pop half a tablet of aspirin into the bottle in the morning - I happen to like the taste of aspirin, don't have any stomach problems, and the 150mg a day of aspirin might be good for my health.

saving

Carni-Festivals I contributed to This Week

What's better than pfblogs.org? Why, the Carnivals and Festivals each week - get all the best posts and none of rest! Enjoy:

12 NOV: Carnival of Investing Week 48 included my Net Worth - PF Bloggers progress for OCT '06 post

14 NOV: Carnival of Wealth Building Ideas included my A Review of ReviewMe.com post

14 NOV: Festival of Frugality #48 included my Frugal living: Recycling Calendars and Diaries post

14 NOV: Festival of Investing included my A Word a Day: "Gearing" post

12 NOV: Carnival of Investing Week 48 included my Net Worth - PF Bloggers progress for OCT '06 post

14 NOV: Carnival of Wealth Building Ideas included my A Review of ReviewMe.com post

14 NOV: Festival of Frugality #48 included my Frugal living: Recycling Calendars and Diaries post

14 NOV: Festival of Investing included my A Word a Day: "Gearing" post

Blog Monetization: Why I love PPP

There are many, many nice things about PayPerPost, the word of mouth marketing service:

1. They pay (I got my first $4.00 paid into my PayPal account a few days ago, so I can vouch for this).

2. They pay a reasonable amount of money per post, so it's actually worthwhile.

3. They have a range of "opportunities" available, and new ones appear all the time.

4. Some of the opportunities are relevant to my readers, as they deal with PF related topics/services, or I can personally relate to the produce, so its worth a blog.

5. They don't mind posts being tagged as sponsored - in fact they encourage it!

6. There are lots of "opportunities" that allow either +ve or -ve comment, so I can write as I see fit. ps. Even if the "opportunity" only wanted +ve reviews, I'd still review it if I had looked into the site and had negative views to express - I just wouldn't take the PPP opportunity and get paid for my comment.

7. The turn around on accepting your posts and approving them for payment is very quick - usually only 1 or 2 days.

8. Their website is very clearly laid out and easy to use.

PayPerPost

1. They pay (I got my first $4.00 paid into my PayPal account a few days ago, so I can vouch for this).

2. They pay a reasonable amount of money per post, so it's actually worthwhile.

3. They have a range of "opportunities" available, and new ones appear all the time.

4. Some of the opportunities are relevant to my readers, as they deal with PF related topics/services, or I can personally relate to the produce, so its worth a blog.

5. They don't mind posts being tagged as sponsored - in fact they encourage it!

6. There are lots of "opportunities" that allow either +ve or -ve comment, so I can write as I see fit. ps. Even if the "opportunity" only wanted +ve reviews, I'd still review it if I had looked into the site and had negative views to express - I just wouldn't take the PPP opportunity and get paid for my comment.

7. The turn around on accepting your posts and approving them for payment is very quick - usually only 1 or 2 days.

8. Their website is very clearly laid out and easy to use.

PayPerPost

A Word a Day: "Liquidity"

The ability of an investment to be converted into cash quickly and with little or no loss in value.

0% CC Balance Transfer Arbitrage

A lot of posts on the Personal Finance blogs have outlined the hows, whys and wherefores of doing a 0% balance transfer Arbitrage to earn interest on OPM. Lots of other blogs deal with those struggling to pay off CC debt, and who could benefit from transferring their current balance to a lower rate CC. But how do you find the best CC available?

I've just had a look at a site which lets you compare the various features of Credit Cards - it even has a page listing cards that have a 0% balance transfer available! All in all this looks like a very useful site for my US readers.

PayPerPost

I've just had a look at a site which lets you compare the various features of Credit Cards - it even has a page listing cards that have a 0% balance transfer available! All in all this looks like a very useful site for my US readers.

PayPerPost

My Investment Loan Interest Rates

While asset allocation is probably the most important factor in your long term investment performance, and fees and charges the second mosst significant item, the interest rate you pay on any investment borrowings are also a major consideration. A few percentage points extra can mean the difference between the use of gearing adding to or reducing your ROI. There can be considerable differences in the interest rates charged by different lenders, so it pays to shop around. Also, there may be price breaks from larger loan balances, so this is a time when diversifying between different lenders can be counter-productive. My investment borrowings are a bit of a mish mash, due to changes in investment stratgey over time, and using new lenders (at cheaper rates) for new investments, while keeping the old accounts in order to not realise capital gains just by shifting assets between accounts.

My investment loans:

* This Line of Credit is used to capitalise margin loan interest prepayment in June, and is then paid off with my tax refund in November.

Overall, the interest rate on my property loans currently averages 7.275%, and the interest rate on my stock portfolio loans currently averages 8.041%. The use of 1-year prepaid interest fixed rate loans helped lower the overall interest rate, as the Reserve Bank has raised rates a couple of times since June. The opportunity cost of prepaying interest for a year can be ignored as prepayment brings forward the tax deduction for the interest payment.

My investment loans:

Property

$230,602.65 @ 7.37% - home loan (non-deductible) - variable rate

$118,250.00 @ 7.09% - rental property loan (deductible) - fixed rate (5 yr term)

Shares - AU - three margin lending accounts

$19,474.16 @ 8.85% - St George Margin Lending (St George Bank) - variable rate

$12,042.90 @ 8.90% - Commonwealth Securities (Commonwealth Bank) - variable rate

$82,065.38 @ 7.95% - Commonwealth Securities (Commonwealth Bank) - fixed rate (1 yr term)

$150,000.00 @ 8.25% - Leveraged Equities (Adelaide Bank) - fixed rate (1 yr term)

$5,607.76 @ 9.15% - Leveraged Equities (Adelaide Bank) - variable rate

Shares - US

$59,175.20 @ 7.09% - St George Portfolio loan (secured against property) - variable rate

Other

$ nil @12.99% - Citibank*

Property

$230,602.65 @ 7.37% - home loan (non-deductible) - variable rate

$118,250.00 @ 7.09% - rental property loan (deductible) - fixed rate (5 yr term)

Shares - AU - three margin lending accounts

$19,474.16 @ 8.85% - St George Margin Lending (St George Bank) - variable rate

$12,042.90 @ 8.90% - Commonwealth Securities (Commonwealth Bank) - variable rate

$82,065.38 @ 7.95% - Commonwealth Securities (Commonwealth Bank) - fixed rate (1 yr term)

$150,000.00 @ 8.25% - Leveraged Equities (Adelaide Bank) - fixed rate (1 yr term)

$5,607.76 @ 9.15% - Leveraged Equities (Adelaide Bank) - variable rate

Shares - US

$59,175.20 @ 7.09% - St George Portfolio loan (secured against property) - variable rate

Other

$ nil @12.99% - Citibank*

* This Line of Credit is used to capitalise margin loan interest prepayment in June, and is then paid off with my tax refund in November.

Overall, the interest rate on my property loans currently averages 7.275%, and the interest rate on my stock portfolio loans currently averages 8.041%. The use of 1-year prepaid interest fixed rate loans helped lower the overall interest rate, as the Reserve Bank has raised rates a couple of times since June. The opportunity cost of prepaying interest for a year can be ignored as prepayment brings forward the tax deduction for the interest payment.

Thursday, 16 November 2006

World's Biggest Double Counting Error?

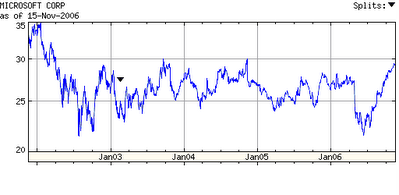

I don't get it - how can W. Gates III still be "the world's richest man" with a NW around US$50b, when this appears to still count the $25b or so he donated to his charitable trust a couple of years ago?. Surely his net worth is now "only" $25b or thereabouts?. Either the money is still his, or else he's donated it to the trust and it isn't "his" anymore.

A quick look at the Microsoft share price since 2001 shows that his net worth probably dropped from $52.8b in 2002 to $40.7b the following year - so he didn't suddently have an extra $24b to donate into his charitable trust - it must have come out of his net worth.

Year NetWorth (Forbes) in Trust (total)

2001 $58,700,000,000 n/a

2002 $52,800,000,000 n/a

2003 $40,700,000,000 $24,000,000,000

2004 $48,000,000,000 $27,000,000,000

2005 $46,500,000,000 $27,000,000,000

2006 $50,000,000,000 $29,000,000,000

A quick look at the Microsoft share price since 2001 shows that his net worth probably dropped from $52.8b in 2002 to $40.7b the following year - so he didn't suddently have an extra $24b to donate into his charitable trust - it must have come out of his net worth.

Blog Monetization update: Nov 2006

My first payment appeared in my PayPal account yesterday! A grand total of USD$4.00 - this exactly covers the pfblogs.org friends fees I've paid so far ;)

Over the next month there should be some more noticeable amounts deposited into PayPal, as my earnings for the past month posts start to become due for payment.

So far total accrued blog earnings are as follows:

I don't have exact visitor stats from launch as I didn't put sitemeter onto my blog until it had been running a while. However, the adsense hits should accurately reflect the # page views, and the page view:visitor ratio seems faily constant around 1.5, so I can estimate the total # visitors.

This works out at about 5c per visitor, or $0.99 per post.

Sadly, with all the time spent fiddling with templates, reading other blogs, researching posts etc. the hourly rate would work out at about 25c an hour. Just as well I'm doing this blog for a bit of fun (and maybe the posts be of some use to others). I would be spending the time reading pf blogs and fiddling with my finances anyhow, so the monetization is just for a bit of fun.

ps. My wife thinks I'm a bit strange to get excited to find out that I earned $2.71 Amazon.com commision (OK, she thinks I'm a bit strange anyhow). Now, if I could just build up my blog readership to include some of the other 4 billion people on this planet I could start making some serious cash out of this internet thingy ;)

pps. Slap me if I ever put one of those PayPal "Tips" buttons on this blog!

Over the next month there should be some more noticeable amounts deposited into PayPal, as my earnings for the past month posts start to become due for payment.

So far total accrued blog earnings are as follows:

Amazon.com $2.71 (1 sale from 64 click thrus)

AdSense $x.xx AdSense earnings are Top Secret (let's just say the x's give you a good indication of scale)

Adbrite $0.00

PayPerPost $82.01 (13 posts)

Blogsvertise $15.00 (3 posts)

ReviewMe $20.00 (1 post)

-------

TOTAL TO DATE: $128.49 EARNED

TOTAL TO DATE: $4.00 PAID (INTO PAYPAL)

Amazon.com $2.71 (1 sale from 64 click thrus)

AdSense $x.xx AdSense earnings are Top Secret (let's just say the x's give you a good indication of scale)

Adbrite $0.00

PayPerPost $82.01 (13 posts)

Blogsvertise $15.00 (3 posts)

ReviewMe $20.00 (1 post)

-------

TOTAL TO DATE: $128.49 EARNED

TOTAL TO DATE: $4.00 PAID (INTO PAYPAL)

I don't have exact visitor stats from launch as I didn't put sitemeter onto my blog until it had been running a while. However, the adsense hits should accurately reflect the # page views, and the page view:visitor ratio seems faily constant around 1.5, so I can estimate the total # visitors.

Blog start date: 19 July 2006

Days running: 120

total posts: 130

total page hits: 3,552

total # visitors: 2,368 (estimated)

Blog start date: 19 July 2006

Days running: 120

total posts: 130

total page hits: 3,552

total # visitors: 2,368 (estimated)

This works out at about 5c per visitor, or $0.99 per post.

Sadly, with all the time spent fiddling with templates, reading other blogs, researching posts etc. the hourly rate would work out at about 25c an hour. Just as well I'm doing this blog for a bit of fun (and maybe the posts be of some use to others). I would be spending the time reading pf blogs and fiddling with my finances anyhow, so the monetization is just for a bit of fun.

ps. My wife thinks I'm a bit strange to get excited to find out that I earned $2.71 Amazon.com commision (OK, she thinks I'm a bit strange anyhow). Now, if I could just build up my blog readership to include some of the other 4 billion people on this planet I could start making some serious cash out of this internet thingy ;)

pps. Slap me if I ever put one of those PayPal "Tips" buttons on this blog!

Wednesday, 15 November 2006

Will Uncle Fred Leave me a Fortune?

I must admit that the question of inheritance doesn't take up much of my time - I expect to have enough accumulated to fund my own retirement, and there's a good chance my parents will still be around when I retire - I have a Great Aunt still alive in her 90s, and two of my Grandparents lived to 94. So if I ever inherit anything I'll probably be too old to enjoy it anyhow.

However, for a lot a Baby Boomers who have been "living in the moment" and are only now starting to get concerned about where the money will come from in their retirement, the possibility of an inheritance bailing them out may have been in the back of their mind.

I had read that this hope was misplaced, with the current crop of retirees planning to spend their money, and possibly use a reverse-mortgage to spend the family home as well. So they'd bit little left for the Baby Boomer's to inherit.

But a new Citibank report contradicts this belief. Apparently most retirees are living within their means and around 85% plan on leaving a bequest to their children.

The average amount expected is $427,000, but some are planning on leaving a lot more:

wealth, retirement

However, for a lot a Baby Boomers who have been "living in the moment" and are only now starting to get concerned about where the money will come from in their retirement, the possibility of an inheritance bailing them out may have been in the back of their mind.

I had read that this hope was misplaced, with the current crop of retirees planning to spend their money, and possibly use a reverse-mortgage to spend the family home as well. So they'd bit little left for the Baby Boomer's to inherit.

But a new Citibank report contradicts this belief. Apparently most retirees are living within their means and around 85% plan on leaving a bequest to their children.

The average amount expected is $427,000, but some are planning on leaving a lot more:

Expected size Proportion of

of Estate Retirees

<$50,000 9%

$50,000 - $199,000 10%

$200,000 - $299,999 17%

$300,000 - $399,999 12%

$400,000 - $499,999 10%

$500,000 - $699,999 10%

$700,000 - $899,999 2%

>$900,000 15%

wealth, retirement

Birth of a new search engine

It's got a cool logo. It's got an interesting angle - country–specific search. Megaglobe is a new international search engine "coming soon". It will be available in 45 langagues and will represent the whole world. (I'm having to take their word for this at this stage.)

Well, that's the buzz.

The reality is that at the moment when you go to Megaglobe - International Search Engine all you see is a submit field where you can enter the web address of a website that you want to be spidered.

Despite a press release dated 23 June which said "Megaglobe will be launched in August" there's not (as yet) any search function. You'd think that a search function would be top of the "to do" list if you're lauching a new search engine... anyhow, the logo looks cool. I said that already, didn't I?

Perhaps, they meant August 2007.

PayPerPost

Well, that's the buzz.

The reality is that at the moment when you go to Megaglobe - International Search Engine all you see is a submit field where you can enter the web address of a website that you want to be spidered.

Despite a press release dated 23 June which said "Megaglobe will be launched in August" there's not (as yet) any search function. You'd think that a search function would be top of the "to do" list if you're lauching a new search engine... anyhow, the logo looks cool. I said that already, didn't I?

Perhaps, they meant August 2007.

PayPerPost

A Word a Day: "Margin Lending"

The use of borrowed funds to purchase securities. It magnifies returns (losses or gains) by reducing the amount of capital an investor must contribute to the investment.

Tuesday, 14 November 2006

My Long Term Net Worth Progress

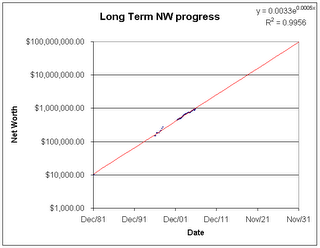

Inspired by MyMoneyBlog's post of his Net Worth progress since his College days, I decided to dig out some old quarterly Net Worth figures I had sitting around from the mid '90s and plot them out. I also remember that I had saved approx. $10,000 working part-time during Uni Vacations (which was spent on a telescope and accessories), so I know that my Net Worth when I started working after graduation in '84 was around $10K.

The striking thing about this plot is how well an exponential trend line fits the data so far - the R^2 ("goodness of fit") value is 0.9956 (an R^2 value of 1.00 would indicate a perfect fit). Extrapolating the trend out to age 70 I would end up with around $100m - worth around $48m in today's AU$. I think this overestimates the end result by a factor of 10 or so - a previous model I'd done based on my expected future savings rate and overall ROI (using the expected ROI of each asset class in my portfolio and my planned use of gearing) ended up with around $4m (in today's AU$) at age 65. I think the main reason for the discrepancy is that up to now my overall rate of increase was significantly boosted by my savings. From now on my annual savings will become insignificant compared to the annual return on my existing portfolio. This will happen to most people as their portfolio experiences compound growth, whereas salary cannot keep going up exponentially.

This is one reason I think Frank the Financially Savvy Atheist's current plan to achieve his targeted Net Worth ($4.5m in 23 years) still needs more work - an assumption of 8% annual pay rises is OK for a new graduate starting out, but I think salary is unlikely to keep increasing at 7% pa by age 46. I think the long term rate of salary rises later in a career is more likely to be around 4%. Perhaps he has some stats specific to his industry/qualifications that support this assumption.

personal finance, wealth, retirement

The striking thing about this plot is how well an exponential trend line fits the data so far - the R^2 ("goodness of fit") value is 0.9956 (an R^2 value of 1.00 would indicate a perfect fit). Extrapolating the trend out to age 70 I would end up with around $100m - worth around $48m in today's AU$. I think this overestimates the end result by a factor of 10 or so - a previous model I'd done based on my expected future savings rate and overall ROI (using the expected ROI of each asset class in my portfolio and my planned use of gearing) ended up with around $4m (in today's AU$) at age 65. I think the main reason for the discrepancy is that up to now my overall rate of increase was significantly boosted by my savings. From now on my annual savings will become insignificant compared to the annual return on my existing portfolio. This will happen to most people as their portfolio experiences compound growth, whereas salary cannot keep going up exponentially.

This is one reason I think Frank the Financially Savvy Atheist's current plan to achieve his targeted Net Worth ($4.5m in 23 years) still needs more work - an assumption of 8% annual pay rises is OK for a new graduate starting out, but I think salary is unlikely to keep increasing at 7% pa by age 46. I think the long term rate of salary rises later in a career is more likely to be around 4%. Perhaps he has some stats specific to his industry/qualifications that support this assumption.

personal finance, wealth, retirement

Xmas Gift Idea: Personalised USB Thumb Drive

I use my USB thumb drive a lot - it's great for backing up your files, transferring files from work to home, or uni to home. These days you there is a large selection of thumb drives with storage capacity of 0.5GB up to 4GB available quite cheaply.

One great idea I've seen is to get one with laser engraving of your name on it in case it gets lost. At the moment Pexagontech.com has 1GB Thumb Drives (in any one of five cool colours) for $20.99 with FREE laser engraving, & 2GB Thumb Drives (any color) for $38.99 with FREE laser engraving. They also offer a service called “myDrive LOST-N-FOUND” where they will engrave your drive with a unique product identification number and store your contact information on their secure database. If your drive gets lost their website has a short form where the finder can enter the unique product identification number, be entitled to a reward and Pexagontech.com will arrange to have the drive returned to you, free of charge!

PayPerPost

One great idea I've seen is to get one with laser engraving of your name on it in case it gets lost. At the moment Pexagontech.com has 1GB Thumb Drives (in any one of five cool colours) for $20.99 with FREE laser engraving, & 2GB Thumb Drives (any color) for $38.99 with FREE laser engraving. They also offer a service called “myDrive LOST-N-FOUND” where they will engrave your drive with a unique product identification number and store your contact information on their secure database. If your drive gets lost their website has a short form where the finder can enter the unique product identification number, be entitled to a reward and Pexagontech.com will arrange to have the drive returned to you, free of charge!

PayPerPost

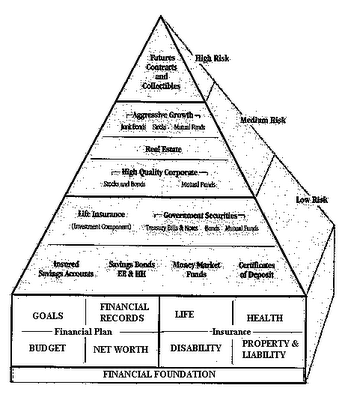

An Very Interesting FREE Home-Study Personal Finance Course

"Investing for your future" is a basic investing home-study course available online. The 11-unit home study course was developed by the Cooperative Extension system for beginning investors with small dollar amounts to invest. It is aimed at those who may be investing for the first time or selecting investment products, such as a stock index fund or unit investment trust, that they have not purchased previously.

It has some valuable information and some cute graphics, such as the "investment pyramid" (reminiscent of the "food pyramid"):

And it also has some exotic terminology that I haven't come across before, such as "loanership"!

All in all, a good read for a cold winter's night in front of the PC with a cup of hot chocolate.

personal finance, investing

It has some valuable information and some cute graphics, such as the "investment pyramid" (reminiscent of the "food pyramid"):

And it also has some exotic terminology that I haven't come across before, such as "loanership"!

All in all, a good read for a cold winter's night in front of the PC with a cup of hot chocolate.

personal finance, investing

He Who Laughs Last

I had an interesting phone call to my "non advisory" financial planner today. The company doesn't actually do any planning for me, I just use them to lodge mutual fund applications as they rebate 100% of the upfront fee (which is generally paid by the mutual fund to their distributors to get them to push product). They profit by getting the trailing fees on the investments (usually around 0.5%)

I'd bought a $50,000 hedge fund investment (Macquarie Equinox Select Opportunities Fund) back in June (using a 100% gearing loan) and prepaid the coming 12 months interest on the loan (so that it was deductible that tax year). As I'd only come across this investment a couple of weeks before the end of the Australian tax year (June 30), I decided to apply directly to the fund manager online, rather than print out the prospectus and mail it in via the "non advisory" financial planner. I thought I'd still be OK to get the entry fee (4%) rebated as the online form asked for your planner's details and what % fee they were to be paid.

However, I hadn't received any rebate yet, so when I sent in the application for my new son's "child super" account to the planner last week (to get the entry fee rebate, and, hopefully a rebate of the trailing commisions) I enquired about the missing rebate from June.

A couple of interesting things turned up - firstly, the fund manager claimed that they had no record of the planner's details from my online application, but that they were happy to send the planner the fee if I emailed them to that effect (I'd then be able to get 80% of the fee rebated back to me, so this was very good).

The second thing, and this is the funny bit, is that after confirming that I could get an 80% rebate of the 4% entry fee on my $50,000 investment made last June (which meant the "non advisory" planner was pocketing $400 for a couple of minutes paperwork, PLUS would get ongoing trailing fees of about $250 pa for doing nothing) he also confirmed that my son's super account application had been forwarded with the entry fee rebate approved (ie 4% of $1000) BUT they hadn't approved the rebate of the trailing commision (around 0.6% per year). I said that a few year's earlier they HAD approved a rebate of the trailing fees on my first son's super account, and as the amount was going to be trivial (around $6 per year!) I didn't think it was a big issue. The "planner" then commented that the trailing fee would just about pay for the express postage they'd paid for my son's paper work to be forwarded to the superannuation fund. At this point I just gave up - why argue about a $6 annual fee when they're going to be pocketing hundreds of dollars each year in trailing fees for my other investments placed via them?

On the bright side, there's another discount broker service that will rebate 50% of the next year's trailing fees if I fill in a form notifying the investment fund that I'm changing to them as my "advisor" - this would mean my current "non-advisory" planner would lose out on any further trailing commisions from my existing investments placed via them (probably worth about $400 a year to them) - all for the sake of not OKing a rebate worth $6 a year. So there!

I'd bought a $50,000 hedge fund investment (Macquarie Equinox Select Opportunities Fund) back in June (using a 100% gearing loan) and prepaid the coming 12 months interest on the loan (so that it was deductible that tax year). As I'd only come across this investment a couple of weeks before the end of the Australian tax year (June 30), I decided to apply directly to the fund manager online, rather than print out the prospectus and mail it in via the "non advisory" financial planner. I thought I'd still be OK to get the entry fee (4%) rebated as the online form asked for your planner's details and what % fee they were to be paid.

However, I hadn't received any rebate yet, so when I sent in the application for my new son's "child super" account to the planner last week (to get the entry fee rebate, and, hopefully a rebate of the trailing commisions) I enquired about the missing rebate from June.

A couple of interesting things turned up - firstly, the fund manager claimed that they had no record of the planner's details from my online application, but that they were happy to send the planner the fee if I emailed them to that effect (I'd then be able to get 80% of the fee rebated back to me, so this was very good).

The second thing, and this is the funny bit, is that after confirming that I could get an 80% rebate of the 4% entry fee on my $50,000 investment made last June (which meant the "non advisory" planner was pocketing $400 for a couple of minutes paperwork, PLUS would get ongoing trailing fees of about $250 pa for doing nothing) he also confirmed that my son's super account application had been forwarded with the entry fee rebate approved (ie 4% of $1000) BUT they hadn't approved the rebate of the trailing commision (around 0.6% per year). I said that a few year's earlier they HAD approved a rebate of the trailing fees on my first son's super account, and as the amount was going to be trivial (around $6 per year!) I didn't think it was a big issue. The "planner" then commented that the trailing fee would just about pay for the express postage they'd paid for my son's paper work to be forwarded to the superannuation fund. At this point I just gave up - why argue about a $6 annual fee when they're going to be pocketing hundreds of dollars each year in trailing fees for my other investments placed via them?

On the bright side, there's another discount broker service that will rebate 50% of the next year's trailing fees if I fill in a form notifying the investment fund that I'm changing to them as my "advisor" - this would mean my current "non-advisory" planner would lose out on any further trailing commisions from my existing investments placed via them (probably worth about $400 a year to them) - all for the sake of not OKing a rebate worth $6 a year. So there!

A Tale of Two Telescopes

A PayPerPost opportunity to blog about telescopes was too good to pass up. I've been an astronomy buff since I was a little kid. I can still remember being taken out of school on the day of the Apollo 11 moon landing to watch it on our black and white TV, and I still get a thrill of space exploration and astronomy.

Back when I was in primary school (about 10) my father had a telescope which I was allowed to use. One windy day I lugged it outside to observe sun spots (using solar projection technique) when it fell over and broke. I then saved up for several years (doing various unpleasant tasks in a market garden, such as "rebagging" rotten potatoes and weeding flower beds or picking green beans in the midday sun, all for 60c and hour) so I could buy myself a Tasco reflecting telescope. It looked a bit like this:

This 'scope lasted me all through high-school, and I loved watching the moons of Jupiter and the rings of Saturn on a clear winter's night. My efforts at astrophotography were never very successful, but I had a ball.

My next 'scope was the "big one" - a 10" Meade SCT. I saved all through my undergraduate uni years doing factory work in the summer vacations to buy that beauty, and I still have it today. One of the good things about a telescope is that one with good optics and mounting will give years of service. I've started showing the heavens to my six year old son with this telescope, and it will probably still be in good working order when he has kids of his own. These days I've traded up from a Pentax MX SLR camera to a Pentax *ist DL digital SLR camera for my astrophotography, but the telescope is still just as good as the day I bought it 20 years ago.

If anyone has a budding astronomer in the familiy, I can't think of a better Christmas gift.

Optics Planet has a huge selection - thousands of optical products in stock from cheap toys to the best top of the line products on sale. Free UPS Shipping for orders over $29.95. Check them out online for Meade, Celestron, Bushnell Telescopes and more.

PayPerPost

Back when I was in primary school (about 10) my father had a telescope which I was allowed to use. One windy day I lugged it outside to observe sun spots (using solar projection technique) when it fell over and broke. I then saved up for several years (doing various unpleasant tasks in a market garden, such as "rebagging" rotten potatoes and weeding flower beds or picking green beans in the midday sun, all for 60c and hour) so I could buy myself a Tasco reflecting telescope. It looked a bit like this:

This 'scope lasted me all through high-school, and I loved watching the moons of Jupiter and the rings of Saturn on a clear winter's night. My efforts at astrophotography were never very successful, but I had a ball.

My next 'scope was the "big one" - a 10" Meade SCT. I saved all through my undergraduate uni years doing factory work in the summer vacations to buy that beauty, and I still have it today. One of the good things about a telescope is that one with good optics and mounting will give years of service. I've started showing the heavens to my six year old son with this telescope, and it will probably still be in good working order when he has kids of his own. These days I've traded up from a Pentax MX SLR camera to a Pentax *ist DL digital SLR camera for my astrophotography, but the telescope is still just as good as the day I bought it 20 years ago.

If anyone has a budding astronomer in the familiy, I can't think of a better Christmas gift.

Optics Planet has a huge selection - thousands of optical products in stock from cheap toys to the best top of the line products on sale. Free UPS Shipping for orders over $29.95. Check them out online for Meade, Celestron, Bushnell Telescopes and more.

PayPerPost

Monday, 13 November 2006

Carnival of Personal Finance #74

The Carnival of Personal Finance #74 is now available for your reading pleasure at A Geek’s World. Out of the 71 posts in this week's Carnival, my contribution was a post about The Benefits of Compulsory Personal Retirement Accounts.

US Shares - "Little Book" Portfolio Update: Nov 06

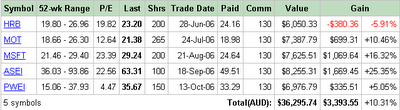

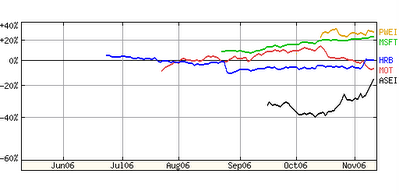

My "Little Book that Beats the Market" Portfolio has progressed nicely this past month, with the gains by ASEI more than offsetting the drop in MOT. I was tempted to sell my Motorola shares when they'd gone up so rapidly and appeared to be dropping back - but my version of the "Little Book" strategy is to hold each stock for 18 months after purchase, then sell and replace with a new pick (unless its still in the short list).

BOUGHT: 150 shares in PW EAGLE, INC. [PWEI] on 13 Oct @ $33.29 - total cost $5,024.29 [AUD $6,758.18] including $65 brokerage.

SOLD: No sale this month (portfolio is in accumulation phase - US$5,000 purchase each month for 18 months)

When selecting which stock to buy I've been keeping clear of commodity (mining & oil) stocks as I think the "e" in their p/e rations may start declining within the next 18 months if commodity prices moderate as production increases meet demand.

PORTFOLIO PERFORMANCE:

I'm currently ahead by 10.62% ($2,642.21) after deducting $65 for selling costs per stock. After deducting approx. $349.00 for interest paid on the loan to date (this portfolio is 100% geared) my total return is currently $2,293.21.

nb. The average gain reported above is spurious as each stock has a different holding period. I'll start tracking net gain (capital gain + dividends - selling costs - interest) once I'm fully invested after 18 months.

personal finance, investing, stocks

BOUGHT: 150 shares in PW EAGLE, INC. [PWEI] on 13 Oct @ $33.29 - total cost $5,024.29 [AUD $6,758.18] including $65 brokerage.

SOLD: No sale this month (portfolio is in accumulation phase - US$5,000 purchase each month for 18 months)

When selecting which stock to buy I've been keeping clear of commodity (mining & oil) stocks as I think the "e" in their p/e rations may start declining within the next 18 months if commodity prices moderate as production increases meet demand.

PORTFOLIO PERFORMANCE:

I'm currently ahead by 10.62% ($2,642.21) after deducting $65 for selling costs per stock. After deducting approx. $349.00 for interest paid on the loan to date (this portfolio is 100% geared) my total return is currently $2,293.21.

nb. The average gain reported above is spurious as each stock has a different holding period. I'll start tracking net gain (capital gain + dividends - selling costs - interest) once I'm fully invested after 18 months.

personal finance, investing, stocks

Sunday, 12 November 2006

Try This Investment Risk Tolerance Quiz

Want to improve your personal finances? You risk tolerance is one of the fundamental issues to consider when planning your investment strategy. Start by taking this quiz from Kansas State University. Choose the response that best describes you - there are no "right" or "wrong" answers. Just have fun!

Take the Quiz

ps. I scored 33 - "a high tolerance for risk", which is what I expected. The score ranges are:

personal finance, investing, risk

Take the Quiz

ps. I scored 33 - "a high tolerance for risk", which is what I expected. The score ranges are:

Score Risk Tolerance Level

0-18 Low tolerance for risk

19-22 Below-average tolerance for risk

23-28 Average/moderate tolerance for risk

29-32 Above-average tolerance for risk

33-47 High tolerance for risk

personal finance, investing, risk

Carni-Festivals My Posts were in This Past Week

What's better than pfblogs.org? Why, the Carnivals and Festivals each week - get all the best posts and none of rest! Enjoy:

06 NOV: Festival of Stock #9 included my AU Shares: T3 Float post

06 NOV: Carnival of Personal Finance #73 included my Will You Live Long Enough to Enjoy your Wealth? post

07 NOV: Festival of Investing included my Money Myths: #1 - Money can’t buy you happiness post

06 NOV: Festival of Stock #9 included my AU Shares: T3 Float post

06 NOV: Carnival of Personal Finance #73 included my Will You Live Long Enough to Enjoy your Wealth? post

07 NOV: Festival of Investing included my Money Myths: #1 - Money can’t buy you happiness post

How to Make an Extra Million for Your Retirement in three easy steps

1. Start when you are 20

2. Earn an extra $3 each and every day

3. Invest it via a regular savings plan with 100% gearing ($100 borrowed for every $100 invested) into the following asset mix: