Until yesterday DW and I were working for the same company, having both started there about 18 years ago. Then yesterday DW was 'offered' a redundancy package. Not much choice in the matter as it was presented as a fait accompli, with her current role being no longer required, and there apparently no other 'fit' found for her. At least the redundancy package was 'generous', adding up to almost 2 years worth of salary and DW was happy enough to sign and clear out her desk the same day. Personally I'm not overly impressed by the 'generosity' of the package, as the 3 weeks x 10 years of service (the maximum counted for redundancy payouts in this state) is pretty much a requirement under state laws, and the payout for unused accumulated annual and long service leave is also mandatory. And the four weeks pay in lieu of 'notice' is also fairly standard, as very few companies these days want workers to stay at work during the required 'notice' period, as they are afraid of disgruntled, laid-off employees getting up to mischief or their presence (dead man walking) being 'bad for morale'. All-in-all the only generous aspect was a couple of extra weeks payment 'ex gratia'.

As DS2 is starting school at his new 'OC' school today, DW is quite happy to be out of work and able to meet him after school. She isn't sure if she will do a TAFE course, have a go at starting up a home business, or just spend more time gardening. Whether or not she 'needs' to get another job will largely depend on whether or not the rental income from her 'off-the-plan' investment unit turns out to be sufficient to cover the interest payments on the 'portfolio loan' (against our home equity) that will be used to pay for the unit upon settlement this coming May-June. As I pay all the household bills her lack of income won't have any immediate impact. In the longer term, if she doesn't get another job she will end up not having as much as expected in her superannuation account to fund her retirement, and she also won't be able to pay down much (any) of the loan balance. If Sydney real estate prices continue to rise over the next decade or so that won't be much of an issue, but if there is a slump in prices she might end up owning a home unit that is worth less than her mortgage...

Of course DW getting laid off immediately made me wonder how secure my own position at the company is - but there isn't really much point worrying about it unless/until it happens. At the moment my role seems fairly secure, but that can easily change, often as a result of decisions made 'behind closed doors' that one is blissfully unaware of until the axe falls. It did prompt me to do a quick spreadsheet model of how I might be tracking with regards to funding my retirement if I was laid off tomorrow, and comparing it with the likely situation if I was laid of next year, or the year after, and so one...

It turns out that, making some reasonable assumptions regarding ongoing contributions rates while I'm still working, and the likely future rates of taxation and earnings on our superannuation investments (I've taken the average rate of return for the past ten years as a 'guesstimate' of possible future returns, given that this is lower than average rate of return for the past three years, or over the entire period of available data), I could 'retire' tomorrow and get a sustainable retirement income of around 80% of my current 'take-home pay' if I sold up my stock portfolio, paid off the margin loans, and added the net amount to my current superannuation balance. This 'sustainable' model assumed that I had to re-contribute around 2% of the fund value every year to allow for inflation, and that the balance of my superannuation account would be run down until there was no residual balance at age 100. (While that may be an optimistic lifespan, my paternal grandparents both lived until 94, and my parents are both alive and well and in their 80s). It also assumed a low rate of tax on superannuation 'pension' payments, which of course is subject to legislative risk.

If I do manage to keep my job for at least another couple of years my sustainable retirement income rises to around 100% of my current 'take-home' pay rate, and working any longer would mean that either a) I can fund a higher rate of 'pension' payments out of my superannuation during retirement, or b) I will be likely to end up with some residual balance, or c) my desired rate of pension will be sustainable even if investment returns are worse than expected, or if there are a couple of years of poor investment performance immediately after I 'retire'.

Of course even if I get laid off tomorrow I could probably find some gainful employment until my intended retirement age - either at some other job (probably involving more work for less pay), or possibly by getting qualified as a financial planner and having a go at starting my own financial planning business...

Subscribe to Enough Wealth. Copyright 2006-2017

Tuesday 31 January 2017

Wednesday 25 January 2017

Bonus and taxes

My first salary 'bonus' is due to be paid early next month, and the HR department sent out a reminder to make any nominations to 'salary sacrifice' the bonus into superannuation be COB today, as any 'salary sacrifice' arrangements must be done prospectively, not retrospectively (after the income has been 'earned'). At face value it obviously makes a lot of sense to receive the bonus payment into superannuation (paying 15% contribution tax) rather than receiving it as a salary payment and paying income tax on it at a marginal rate of, say, 37%. On a 5% bonus for a $100K salary, the tax saving achieved via 'salary sacrifice' could be $1100. Looking at it another way, that means the 'after tax' bonus amount would be nearly 35% greater when paid into superannuation compared to taking it as a cash payment.

However, the individual decision regarding whether to 'salary sacrifice' the bonus isn't so simple. For example, DW is on a lower annual salary package, and only works 3 days a week, so her marginal tax rate would be 32.5%, and not 37%, which makes the tax incentive to lock away this money until retirement a lot less enticing. She also has a large settlement payment on an investment home unit due in the middle of this year, so any additional amount she puts into superannuation via salary sacrifice would add to her mortgage balance.

Even in my case I can't simply nominate to 'sacrifice' the entire bonus amount into superannuation, as I already have a sizable 'salary sacrifice' arrangement in place, and the 'cap' on concessionally taxed superannuation contributions might come into play. For my age group, the 'cap' this financial year is $35K (it will reduce to only $25K from 20017-18 onwards unless there are further changes announced in the May budget), and I already have around $9.5K of SGL contributions and $19.2K of existing 'salary sacrifice' arrangements. This would mean that around $6.3K more could be 'sacrificed' into superannuation this financial year without exceeding the 'cap'. However, I have to allow for the possibility of a small increase in SGL contributions during the remainder of this financial year if I happen to get a pay rise (annual salary reviews are also being announced next month - just after bonuses get paid out), and there was a monthly employer contribution deposited on 1/7/2016, so I have to allow for the possibility that the contribution for June 2017 might get deposited at the end of June, meaning 13 monthly contributions falling into this FY.

Finally, my employer is also reimbursing small amounts for the monthly admin fee and insurance premium that gets initially debited from my superannuation account (~$85 per month), but the reimbursement payments get processed several months after the original debit transactions. There was a delay in the initial reimbursement payments (eg. a debit processed last FY (on 3/3) was eventually reimbursed via an additional employer superannuation contribution this FY (on 17/10), and there are currently two reimbursement payments being deposited each month in order to 'catch up'. So there *might* be as many as 18 lots of ~$85 deposited this FY, Which means allowing for another $3.8K or so that *might* be deposited this FY and count towards the 'cap'. So, the maximum amount of bonus I can 'salary sacrifice' and be reasonably certain that I won't exceed the 'cap' on concessionally taxed contributions is only $2.5K. In the end I decided to request that $2K of any bonus amount be paid as 'salary sacrifice'.

Next FY I'll have to reduce the amount of monthly 'salary sacrifice' due to the decrease in 'cap'. I probably won't bother to allow for any bonus to be processed via salary sacrifice next year.

Subscribe to Enough Wealth. Copyright 2006-2017

However, the individual decision regarding whether to 'salary sacrifice' the bonus isn't so simple. For example, DW is on a lower annual salary package, and only works 3 days a week, so her marginal tax rate would be 32.5%, and not 37%, which makes the tax incentive to lock away this money until retirement a lot less enticing. She also has a large settlement payment on an investment home unit due in the middle of this year, so any additional amount she puts into superannuation via salary sacrifice would add to her mortgage balance.

Even in my case I can't simply nominate to 'sacrifice' the entire bonus amount into superannuation, as I already have a sizable 'salary sacrifice' arrangement in place, and the 'cap' on concessionally taxed superannuation contributions might come into play. For my age group, the 'cap' this financial year is $35K (it will reduce to only $25K from 20017-18 onwards unless there are further changes announced in the May budget), and I already have around $9.5K of SGL contributions and $19.2K of existing 'salary sacrifice' arrangements. This would mean that around $6.3K more could be 'sacrificed' into superannuation this financial year without exceeding the 'cap'. However, I have to allow for the possibility of a small increase in SGL contributions during the remainder of this financial year if I happen to get a pay rise (annual salary reviews are also being announced next month - just after bonuses get paid out), and there was a monthly employer contribution deposited on 1/7/2016, so I have to allow for the possibility that the contribution for June 2017 might get deposited at the end of June, meaning 13 monthly contributions falling into this FY.

Finally, my employer is also reimbursing small amounts for the monthly admin fee and insurance premium that gets initially debited from my superannuation account (~$85 per month), but the reimbursement payments get processed several months after the original debit transactions. There was a delay in the initial reimbursement payments (eg. a debit processed last FY (on 3/3) was eventually reimbursed via an additional employer superannuation contribution this FY (on 17/10), and there are currently two reimbursement payments being deposited each month in order to 'catch up'. So there *might* be as many as 18 lots of ~$85 deposited this FY, Which means allowing for another $3.8K or so that *might* be deposited this FY and count towards the 'cap'. So, the maximum amount of bonus I can 'salary sacrifice' and be reasonably certain that I won't exceed the 'cap' on concessionally taxed contributions is only $2.5K. In the end I decided to request that $2K of any bonus amount be paid as 'salary sacrifice'.

Next FY I'll have to reduce the amount of monthly 'salary sacrifice' due to the decrease in 'cap'. I probably won't bother to allow for any bonus to be processed via salary sacrifice next year.

Subscribe to Enough Wealth. Copyright 2006-2017

Took up part of my Santos Share Purchase Plan entitlement

I decided to purchase $5000 worth of Santos shares under the SPP that closes next week (31 Jan). The issue price will be around $4.00. As I also have some long crude oil CFDs, I'm obviously punting on the oil price going back up a bit in future. My current holding of Santos shares is around $15,000 market value, so this will increase my investment in Santos by around 1/3. While the oil price has fluctuated wildly over the past 30 years (from below $20 to over $140!), there seems to be some support around the $40 mark, which corresponds roughly to a Santos share price around $4.00. So, overall, it seems that the downside risk is for the share price drop to as low as $2 (or the company to go broke in a period of prolonged low oil prices), whereas a continuation in the current rise in oil prices (if there is stronger global growth in future) could see oil hit $60-$80 again, and the Santos stock price rise to $6-$8 again. While this share purchase is a bit of a gamble, as the amount only represents about 1% of my geared stock portfolio, and 1/4% of my net worth, so either outcome won't have a big impact on my net worth.

The top chart below shows the crude oil price (http://www.macrotrends.net/1369/crude-oil-price-history-chart) over the past 30 years, and the bottom chart is the Santos stock price since 1988.

Subscribe to Enough Wealth. Copyright 2006-2017

The top chart below shows the crude oil price (http://www.macrotrends.net/1369/crude-oil-price-history-chart) over the past 30 years, and the bottom chart is the Santos stock price since 1988.

Subscribe to Enough Wealth. Copyright 2006-2017

Buy, Sell or Hold? Who knows...

With the recent run-up in the US stock market, my boss has recently been moving his (and his parent's) investments out of equities and into 'cash'. He claims he moved out of equities and into cash in early 2007, so perhaps he knows what he's doing? However, while the US market certainly looks similar to the pre-crash phases seen in the dot-com bubble from 1996-2000, and the 'frothiness' seen in 2006-2007 just before the GFC, the Australian market looks quite unremarkable at the moment.

So, I'm not about to liquidate my stock portfolio (in fact I recently bought $10K worth of the Vanguard Australian Shares Index ETF (VAS)). However, if the US stock market does suffer a large 'correction' in the next year or so the Australian share market may well drop a bit also - but I'll probably view that as a buying opportunity. Looking at the graph comparing the All Ords and the S&P it is clear that the long-term trend (at least in Australia) has been for a fairly steady rise over the decades, but that there have been many substantial deviations both above and below the trend line. If you are heavily into stocks, deviations well above the trend line are probably a good opportunity to reduce exposure to equities (or at least reduce gearing), and deviations substantially below the trend line are good times to move any available cash into equities. Bearing in mind, of course, your personal risk tolerance and chosen long-term asset allocation.

However, human nature dictates that many people will be tempted to start investing in the market during bull runs, and then move into cash after a stock market crash - exactly contrary to what logic dictates.

Subscribe to Enough Wealth. Copyright 2006-2017

Subscribe to Enough Wealth. Copyright 2006-2017

So, I'm not about to liquidate my stock portfolio (in fact I recently bought $10K worth of the Vanguard Australian Shares Index ETF (VAS)). However, if the US stock market does suffer a large 'correction' in the next year or so the Australian share market may well drop a bit also - but I'll probably view that as a buying opportunity. Looking at the graph comparing the All Ords and the S&P it is clear that the long-term trend (at least in Australia) has been for a fairly steady rise over the decades, but that there have been many substantial deviations both above and below the trend line. If you are heavily into stocks, deviations well above the trend line are probably a good opportunity to reduce exposure to equities (or at least reduce gearing), and deviations substantially below the trend line are good times to move any available cash into equities. Bearing in mind, of course, your personal risk tolerance and chosen long-term asset allocation.

However, human nature dictates that many people will be tempted to start investing in the market during bull runs, and then move into cash after a stock market crash - exactly contrary to what logic dictates.

Monday 23 January 2017

Diet & Exercise update - 2017 Weeks 2-3

I hadn't managed to get back into the swing of sticking to my diet plan, so my weight continued to creep up for the past couple of weeks. Aside from eating some junk food, I think a lack of exercise due to the recent run of hot (38C+) and humid weather hasn't helped - I haven't been going for long walks at lunchtime or in the evenings, or doing my weekend session of squash with the kids while they were staying with my parents up at the lake house.

Now the kids are back in Sydney and school term is about to start, things should settle back into the normal routine. I managed to get the pool filter working again last week, and finished cleaning the pool on the weekend, so I'll do some laps after work if it is too hot to go for a walk.

. Fibre Carbs Fat Protein kCals Avg Wt Steps

g/dy % % g/dy /dy kg /dy

2017

Week 01 41.4 58.8 21.0 136.7 3,134 97.2 5,368

Week 02 43.4 63.7 17.0 126.1 3,022 97.7 5,259

Week 03 38.4 63.3 18.7 128.8 2,972 98.1 5,931

Subscribe to Enough Wealth. Copyright 2006-2017

Now the kids are back in Sydney and school term is about to start, things should settle back into the normal routine. I managed to get the pool filter working again last week, and finished cleaning the pool on the weekend, so I'll do some laps after work if it is too hot to go for a walk.

. Fibre Carbs Fat Protein kCals Avg Wt Steps

g/dy % % g/dy /dy kg /dy

2017

Week 01 41.4 58.8 21.0 136.7 3,134 97.2 5,368

Week 02 43.4 63.7 17.0 126.1 3,022 97.7 5,259

Week 03 38.4 63.3 18.7 128.8 2,972 98.1 5,931

Subscribe to Enough Wealth. Copyright 2006-2017

Friday 20 January 2017

Benchmarking my NW performance

My usual benchmark for NW performance is to compare it to the 'cut-off' NW reported in the annual BRW 'rich list'. However, that benchmark has a couple of deficiencies:

- the cut-off is for a fixed number of 'richest' Australians, which due to population growth becomes a more and more selective group, hence pushing up the 'cut-off'

- the NW estimates in the 'rich list' are estimates of debatable accuracy

I therefore view it as more of an aspirational target than a realistic benchmark of my NW performance.

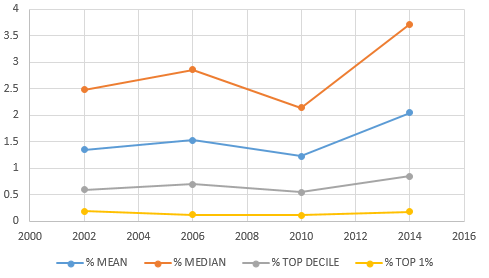

The annual HILDA report that came out last year offers a more robust metric for comparison - Table 5.1 in the report provides Australian household net worth estimates (based on a statistically significant sample), for the years 2002, 2006, 2010 and 2014. The values of mean, median, top10% and top1% are provided in '2014' dollars (ie. adjusted for inflation).

For comparison purposes I used my monthly NW estimate from networthiq.org to calculate my average annual NW figures, and then used the online inflation calculator from the ABS to calculate the equivalent values in constant 2014 dollars.

Plotting these NW values against the mean, median, top decile, and top "1%" figures from the HILDA report show that my NW suffered more from the GFC (due to my use of gearing in my stock portfolio I presume), but bounced back by 2014. However, while my relative NW increased substantially vs. the mean (up 51%), median (up 50%) and top deciles (up 44%) between 2002 and 2014, it barely 'kept pace' with the household NW reported for the top "1%".

But looking at the 2010 figures, my relative performance was down slightly vs. the mean (down 9%), median (down 14%), and top decile (down 8%) groups, but substantially worse that for the top "1%" (down 43%). So I'm hopeful that going forward my NW should also gain ground vs. the 'top 1%' metric. I'll have to wait until the 2020 HILDA report to find out!

Subscribe to Enough Wealth. Copyright 2006-2017

- the cut-off is for a fixed number of 'richest' Australians, which due to population growth becomes a more and more selective group, hence pushing up the 'cut-off'

- the NW estimates in the 'rich list' are estimates of debatable accuracy

I therefore view it as more of an aspirational target than a realistic benchmark of my NW performance.

The annual HILDA report that came out last year offers a more robust metric for comparison - Table 5.1 in the report provides Australian household net worth estimates (based on a statistically significant sample), for the years 2002, 2006, 2010 and 2014. The values of mean, median, top10% and top1% are provided in '2014' dollars (ie. adjusted for inflation).

For comparison purposes I used my monthly NW estimate from networthiq.org to calculate my average annual NW figures, and then used the online inflation calculator from the ABS to calculate the equivalent values in constant 2014 dollars.

Plotting these NW values against the mean, median, top decile, and top "1%" figures from the HILDA report show that my NW suffered more from the GFC (due to my use of gearing in my stock portfolio I presume), but bounced back by 2014. However, while my relative NW increased substantially vs. the mean (up 51%), median (up 50%) and top deciles (up 44%) between 2002 and 2014, it barely 'kept pace' with the household NW reported for the top "1%".

But looking at the 2010 figures, my relative performance was down slightly vs. the mean (down 9%), median (down 14%), and top decile (down 8%) groups, but substantially worse that for the top "1%" (down 43%). So I'm hopeful that going forward my NW should also gain ground vs. the 'top 1%' metric. I'll have to wait until the 2020 HILDA report to find out!

Subscribe to Enough Wealth. Copyright 2006-2017

Thursday 19 January 2017

Adapting William J. Bernstein's book "If You Can" for Young Australians

After dabbling with stock picking and then fund/fund manager picking (and not doing very well at either), I eventually arrived at the same sort of conclusions as William J. Bernstein - pick a suitable asset allocation and invest via low-cost 'index' funds. He recently published a nice small volume of investment advice for 'Millennials', but it is a bit too 'US-centric' (eg. 401K plans and so on) to be immediately applied by young Australian investors. With that in mind, I decided to have a look at how the principles expressed in Bernstein's book could be employed by my sons when they start a career and begin to think about saving and investing.

In a nut-shell, Bernstein's advice for (US) Millennials is simply to:

* save 15% of your (pre-tax) salary annually, and invest it.

* invest it in equal proportions in: domestic stock market index fund, international stock market index fund, and domestic bond market index fund.

* rebalance each year to maintain equal proportions in these three asset classes.

For Australians, the tax system provides substantial benefits for investing inside superannuation. And 9.5% of salary is directed automatically intro superannuation via the 'SGL' (superannuation guarantee levy) for most employees. This can be 'topped up' to the 15% target by arranging to have another 5.5% (or more) of salary directed into superannuation via 'salary sacrifice' (bearing in mind the $30K pa 'cap' on concessionaly taxed contributions (SGL+SS))

However, for Australians, the plan's assumption that half of retirement income needs will eventually come from 'social security' isn't correct, as our 'aged pension' system is both means and assets tested (and while the US social security system in underfunded, our aged pension system is completely unfunded - relying on current tax payers to pay for the aged pensions of retirees -- not a great situation given the aging population and shrinking proportion of taypers:retirees). So perhaps the required rate of savings for Australian Millennials needs to be a bit closer to 30% of salary than 15%. (But this isn't quite as bad as it seems, given that US workers also have around 7.65% deducted for social security and medicare).

Now, in terms of how to invest those savings in the proportions suggested by Bernstein, one could invest in the Vanguard 'growth' index fund, which has the following 'target' (strategic) asset allocation:

35% domestic stocks/property:

Vanguard Australian Shares Index Fund (Wholesale) 31.0%

Vanguard Australian Property Securities Index Fund (Wholesale) 4.0%

35% international stocks/property:

Vanguard International Shares Index Fund (Wholesale) 24.0%

Vanguard International Property Securities Index Fund (Hedged) (Wholesale) 4.0%

Vanguard International Small Companies Index Fund (Wholesale) 3.5%

Vanguard Emerging Markets Shares Index Fund (Wholesale) 3.5%

30% fixed interest:

Vanguard Australian Fixed Interest Index Fund (Wholesale) 12.0%

Vanguard International Fixed Interest Index Fund (Hedged) (Wholesale) 12.0%

Vanguard International Credit Securities Index Fund (Hedged) (Wholesale) 6.0%

nb. Fees: 0.90% on first $50K, 0.60% on next $50K, then 0.35% on balance over $100K.

This is fairly close to the recommended three-way equal split, and would not require any rebalancing as the fund automatically maintains the asset allocation within a fairly tight band. Some of the growth asset allocation is into 'property' rather than shares, but over the long term that should not have much impact on overall return, and may add some additional diversification benefit.

Alternatively, Australian investors could invest in the relevant Vanguard listed ETFs to get the desired asset allocation. Some examples:

VGS: MSCI World ex-Australia

VTS: CRSP US Total Market Index

VUE: FTSE All-World ex US Index

VAF: Bloomberg AusBond Bank Bill Index

VSO: MSCI Australian Shares Small Cap Index

VLC: MSCI AUstralian Shares Large Cap Index

VAS: S&P/ASX 300 Index

However, while the management costs are low (0.05% - 0.30% pa), there may also be a cost to purchase the ETFs via a broker (eg. CommSec), which would rule out making multiple, small purchases on a regular basis. One disincentive to moving out of the 'growth' index fund and into a mixture of ETFs is that some capital gains might be realized (although the rate of capital gains tax is fairly low within a SMSF).

Once DS1 is old enough to become a member/trustee of our SMSF, I'll add him to our SMSF and arrange for his current 'retail' superannuation fund balance to be 'rolled over' into our SMSF. Our SMSF doesn't quite have the asset allocation recommended by Bernstein - it has around 4% invested in cash (in an ANZ V2Plus account paying a silly 0.75%) to provide a 'float' for any SMSF tax bills, and the rest is invested in the Vanguard Lifestrategy 'High Growth' fund. The fund is around 90% invested in 'growth' assets, and only 10% invested in fixed interest. By the time DS1 finishes uni (he is only doing his HSC this year, and plans on doing a 5-year 'double degree' and possible then a 1.5 year masters) and has substantial superannuation contributions flowing into our SMSF, both DW and I will be close to retirement, so we may review the SMSF asset allocation at that time. Once the bulk of the SMSF is in 'pension mode' any capital gains tax implications arising from moving out of one Vanguard Fund into another will be insignificant.

Subscribe to Enough Wealth. Copyright 2006-2017

In a nut-shell, Bernstein's advice for (US) Millennials is simply to:

* save 15% of your (pre-tax) salary annually, and invest it.

* invest it in equal proportions in: domestic stock market index fund, international stock market index fund, and domestic bond market index fund.

* rebalance each year to maintain equal proportions in these three asset classes.

For Australians, the tax system provides substantial benefits for investing inside superannuation. And 9.5% of salary is directed automatically intro superannuation via the 'SGL' (superannuation guarantee levy) for most employees. This can be 'topped up' to the 15% target by arranging to have another 5.5% (or more) of salary directed into superannuation via 'salary sacrifice' (bearing in mind the $30K pa 'cap' on concessionaly taxed contributions (SGL+SS))

However, for Australians, the plan's assumption that half of retirement income needs will eventually come from 'social security' isn't correct, as our 'aged pension' system is both means and assets tested (and while the US social security system in underfunded, our aged pension system is completely unfunded - relying on current tax payers to pay for the aged pensions of retirees -- not a great situation given the aging population and shrinking proportion of taypers:retirees). So perhaps the required rate of savings for Australian Millennials needs to be a bit closer to 30% of salary than 15%. (But this isn't quite as bad as it seems, given that US workers also have around 7.65% deducted for social security and medicare).

Now, in terms of how to invest those savings in the proportions suggested by Bernstein, one could invest in the Vanguard 'growth' index fund, which has the following 'target' (strategic) asset allocation:

35% domestic stocks/property:

Vanguard Australian Shares Index Fund (Wholesale) 31.0%

Vanguard Australian Property Securities Index Fund (Wholesale) 4.0%

35% international stocks/property:

Vanguard International Shares Index Fund (Wholesale) 24.0%

Vanguard International Property Securities Index Fund (Hedged) (Wholesale) 4.0%

Vanguard International Small Companies Index Fund (Wholesale) 3.5%

Vanguard Emerging Markets Shares Index Fund (Wholesale) 3.5%

30% fixed interest:

Vanguard Australian Fixed Interest Index Fund (Wholesale) 12.0%

Vanguard International Fixed Interest Index Fund (Hedged) (Wholesale) 12.0%

Vanguard International Credit Securities Index Fund (Hedged) (Wholesale) 6.0%

nb. Fees: 0.90% on first $50K, 0.60% on next $50K, then 0.35% on balance over $100K.

This is fairly close to the recommended three-way equal split, and would not require any rebalancing as the fund automatically maintains the asset allocation within a fairly tight band. Some of the growth asset allocation is into 'property' rather than shares, but over the long term that should not have much impact on overall return, and may add some additional diversification benefit.

Alternatively, Australian investors could invest in the relevant Vanguard listed ETFs to get the desired asset allocation. Some examples:

VGS: MSCI World ex-Australia

VTS: CRSP US Total Market Index

VUE: FTSE All-World ex US Index

VAF: Bloomberg AusBond Bank Bill Index

VSO: MSCI Australian Shares Small Cap Index

VLC: MSCI AUstralian Shares Large Cap Index

VAS: S&P/ASX 300 Index

However, while the management costs are low (0.05% - 0.30% pa), there may also be a cost to purchase the ETFs via a broker (eg. CommSec), which would rule out making multiple, small purchases on a regular basis. One disincentive to moving out of the 'growth' index fund and into a mixture of ETFs is that some capital gains might be realized (although the rate of capital gains tax is fairly low within a SMSF).

Once DS1 is old enough to become a member/trustee of our SMSF, I'll add him to our SMSF and arrange for his current 'retail' superannuation fund balance to be 'rolled over' into our SMSF. Our SMSF doesn't quite have the asset allocation recommended by Bernstein - it has around 4% invested in cash (in an ANZ V2Plus account paying a silly 0.75%) to provide a 'float' for any SMSF tax bills, and the rest is invested in the Vanguard Lifestrategy 'High Growth' fund. The fund is around 90% invested in 'growth' assets, and only 10% invested in fixed interest. By the time DS1 finishes uni (he is only doing his HSC this year, and plans on doing a 5-year 'double degree' and possible then a 1.5 year masters) and has substantial superannuation contributions flowing into our SMSF, both DW and I will be close to retirement, so we may review the SMSF asset allocation at that time. Once the bulk of the SMSF is in 'pension mode' any capital gains tax implications arising from moving out of one Vanguard Fund into another will be insignificant.

Subscribe to Enough Wealth. Copyright 2006-2017

Tuesday 17 January 2017

My current Portfolio of ASX listed investments

I'm a fairly passive investor in the stock market, so aside from some small changes in holding quantities due to dividend reinvestment plans, the only substantial changes since I last posted my stock portfolio details in 2015 are a large decrease in the value of my IPE holding (due to some substantial returns of capital as the fund is slowly wound up), and the liqudation of my holding in the Berkshire ETS last year. I also added small holdings of AFI and ARG in mid 2016, which are both listed investment companies, in order to reinvest some of the cash into the market.

LEML account: (17.JAN.17)

CODE QTY Company Name Mkt Price Mkt Value

AGL 1035 AGL Energy Ltd A$22.03 A$ 22,801.05

ANN 480 Ansell Ltd A$24.25 A$ 11,640.00

ANZ 2149 ANZ Banking Ltd A$30.04 A$ 65,329.60

BHP 748 BHP Billiton Ltd A$26.92 A$ 20,136.16

CYB 236 CYBG PLC A$ 4.67 A$ 1,102.12

NAB 1013 National Aust Bank A$30.73 A$ 31,129.49

QBE 1572 QBE Insurance Ltd A$12.295 A$ 19,327.74

S32 748 South32 Limited A$ 2.81 A$ 2,101.88

TWE 1250 Treasury Wine Estate A$10.43 A$ 13,037.50

------------

Market Value sub-total A$186,605.54

CSML account:

AFI 5000 Australian Foundation A$ 5.93 A$ 29,650.00

ARG 4000 Argo Investment A$ 7.61 A$ 30,440.00

IFL 2000 IOOF Holdings A$ 9.26 A$ 18,520.00

IHD 1000 IShares ASX Div Opport A$13.86 A$ 13,860.00

IPE 244000 IPE Limited A$ 0.17 A$ 41,480.00

RDV 500 Russel High Div Au Shrs A$29.99 A$ 14,995.00

STO 3750 Santos Limited A$ 4.06 A$ 15,225.00

WBC 490 Westpac Banking Corp A$32.75 A$ 16,047.50

WPL 239 Woodside Petroleum A$32.02 A$ 7,652.78

------------

Market Value sub-total A$187,870.28

============

Market Value total A$374,475.82

Subscribe to Enough Wealth. Copyright 2006-2017

LEML account: (17.JAN.17)

CODE QTY Company Name Mkt Price Mkt Value

AGL 1035 AGL Energy Ltd A$22.03 A$ 22,801.05

ANN 480 Ansell Ltd A$24.25 A$ 11,640.00

ANZ 2149 ANZ Banking Ltd A$30.04 A$ 65,329.60

BHP 748 BHP Billiton Ltd A$26.92 A$ 20,136.16

CYB 236 CYBG PLC A$ 4.67 A$ 1,102.12

NAB 1013 National Aust Bank A$30.73 A$ 31,129.49

QBE 1572 QBE Insurance Ltd A$12.295 A$ 19,327.74

S32 748 South32 Limited A$ 2.81 A$ 2,101.88

TWE 1250 Treasury Wine Estate A$10.43 A$ 13,037.50

------------

Market Value sub-total A$186,605.54

CSML account:

AFI 5000 Australian Foundation A$ 5.93 A$ 29,650.00

ARG 4000 Argo Investment A$ 7.61 A$ 30,440.00

IFL 2000 IOOF Holdings A$ 9.26 A$ 18,520.00

IHD 1000 IShares ASX Div Opport A$13.86 A$ 13,860.00

IPE 244000 IPE Limited A$ 0.17 A$ 41,480.00

RDV 500 Russel High Div Au Shrs A$29.99 A$ 14,995.00

STO 3750 Santos Limited A$ 4.06 A$ 15,225.00

WBC 490 Westpac Banking Corp A$32.75 A$ 16,047.50

WPL 239 Woodside Petroleum A$32.02 A$ 7,652.78

------------

Market Value sub-total A$187,870.28

============

Market Value total A$374,475.82

Subscribe to Enough Wealth. Copyright 2006-2017

Tuesday 10 January 2017

Diet & Exercise update - 2017 Week 1

Well, although I managed to follow my diet plan for the first five days of 2017, averaging 2,448 kcals/day, I then ate way too much on the three days I was visiting my parents at our lake house. I also didn't walk very much while at the farm (although I did a couple of hours tractor driving slashing overgrown paddocks). So overall 'week 1' of 2017 was rather mediocre, with too many kcals/day energy intake and not enough walking. And didn't play squash on the weekends we were out of town. The weather has been too hot and humid to go for long walks at lunchtime (or even in the evenings), and unfortunately to pool pump and salt chlorinator have been playing up again, so our pool is a bit too 'green' to swim laps after work. I spend some time acid washing the salt chlorinator sensor on Sunday, and hopefully that gets the pump working again and I can give the pool thorough clean up.

I have three air pistol competitions coming up in February/March, so I need to make sure I start doing SCATT training and 5BX every day.

. Fibre Carbs Fat Protein kCals Avg Wt Steps

g/dy % % g/dy /dy kg /dy

Week 41 42.2 65.9 16.8 120.9 3,107 96.2 9,767

Week 42 43.3 62.6 22.3 129.5 3,488 97.3 5,317

Week 43 40.8 53.5 24.7 108.3 2,755 97.0 6,007

Week 44 36.9 52.4 24.1 97.1 2,856 97.1 4,481

2017

Week 01 41.4 58.8 21.0 136.7 3,134 97.2 5,368

Subscribe to Enough Wealth. Copyright 2006-2017

I have three air pistol competitions coming up in February/March, so I need to make sure I start doing SCATT training and 5BX every day.

. Fibre Carbs Fat Protein kCals Avg Wt Steps

g/dy % % g/dy /dy kg /dy

Week 41 42.2 65.9 16.8 120.9 3,107 96.2 9,767

Week 42 43.3 62.6 22.3 129.5 3,488 97.3 5,317

Week 43 40.8 53.5 24.7 108.3 2,755 97.0 6,007

Week 44 36.9 52.4 24.1 97.1 2,856 97.1 4,481

2017

Week 01 41.4 58.8 21.0 136.7 3,134 97.2 5,368

Subscribe to Enough Wealth. Copyright 2006-2017

Thursday 5 January 2017

Why Aussie share investors hate US share investors

Well, not actually hate them, just envious.

As can be seen in the chart below, Investors in the Aussie share market have basically gone nowhere since the start of 2007. That's right, practically 0% gain over the past decade. In comparison, despite the impact of the GFC (which the US caused, just to rub salt in the wound) the US S&P-500 index has made a respectable 60% or so gain since the start of 2007. Go figure.

Sure the Australian 'mining boom' came to end during the past decade. And the economy suffered a lot from the GFC. But even so, we haven't had a recession for more than a quarter of a century, and our GDP is actually up considerably since the GFC. In fact, the Australia stock market since the GFC has performed eerily like it did during the Great Depression.

To make matters worse, I invested shares with gearing, so I've been paying interest for the privilege of making no money for the past decade! And DW is more interested in property investing than the stock market, so I can't even whinge about the poor stock market performance without getting an "I told you so" ;)

source: http://www.treasury.gov.au/ - 19th Annual Colin Clark Memorial Lecture

source: http://www.treasury.gov.au/ - 19th Annual Colin Clark Memorial Lecture

Subscribe to Enough Wealth. Copyright 2006-2017

As can be seen in the chart below, Investors in the Aussie share market have basically gone nowhere since the start of 2007. That's right, practically 0% gain over the past decade. In comparison, despite the impact of the GFC (which the US caused, just to rub salt in the wound) the US S&P-500 index has made a respectable 60% or so gain since the start of 2007. Go figure.

Sure the Australian 'mining boom' came to end during the past decade. And the economy suffered a lot from the GFC. But even so, we haven't had a recession for more than a quarter of a century, and our GDP is actually up considerably since the GFC. In fact, the Australia stock market since the GFC has performed eerily like it did during the Great Depression.

To make matters worse, I invested shares with gearing, so I've been paying interest for the privilege of making no money for the past decade! And DW is more interested in property investing than the stock market, so I can't even whinge about the poor stock market performance without getting an "I told you so" ;)

Subscribe to Enough Wealth. Copyright 2006-2017

I bought a raffle ticket

While I usually don't gamble, I couldn't resist the temptation to buy a $10 raffle ticket being sold be Cessnock Pistol Club (to be drawn at the Nationals in April). I saw their ad for the raffle while processing my entry in the ISSF Vintage competition (not sure why it is called 'vintage') being held next month. As they are only selling 400 raffle tickets, and the prize is a voucher for a $3600 Pardini pistol, each ticket is notionally 'worth' 1/400 x $3600 = $9. So the cost of $10 seems reasonable. Most lotteries payout around 50%-70% of their ticket sales revenue in prizes, so a $1.30 'Oz Lotto' ticket, for example, is only 'worth' around 80c on average. Of course the reality is that there is a 99.75% probability (399/400) that I've simply thrown that $10 away ;)

If my air pistol results at competitions this year warrant it, I am thinking about upgrading my ~30 year old Feinwerkbau model 100 air pistol - possibly getting the new Steyr Evo 10 air pistol (which replaces the Steyr LP10 that seems to have been the most popular choice at World Cup, Olympic and Commonwealth Games air pistol competitions in recent years). I checked with the company that will be redeeming the raffle prize voucher, and it can be redeemed for any pistol of similar price. So, if I do happen to win the raffle, it would save me having to spend ~$3000 for a new air pistol.

Subscribe to Enough Wealth. Copyright 2006-2017

If my air pistol results at competitions this year warrant it, I am thinking about upgrading my ~30 year old Feinwerkbau model 100 air pistol - possibly getting the new Steyr Evo 10 air pistol (which replaces the Steyr LP10 that seems to have been the most popular choice at World Cup, Olympic and Commonwealth Games air pistol competitions in recent years). I checked with the company that will be redeeming the raffle prize voucher, and it can be redeemed for any pistol of similar price. So, if I do happen to win the raffle, it would save me having to spend ~$3000 for a new air pistol.

Subscribe to Enough Wealth. Copyright 2006-2017

Tuesday 3 January 2017

Net Worth: December 2016

Happy New Year! The Trump/Santa Claus Effect saw global share markets continue to appreciate during December, resulting in my geared stock portfolio and my retirement savings each increase by more than $30K during December. There was no price data available for our suburb (apparently due to few people willing to sell their properties while the hospital precinct rezoning is being finalized, rather than a lack of buyers), so our 'estimated' price for our home was unchanged last month. As I didn't make any capital improvements to my rural property, than too saw its 'book' price remain unchanged.

Overall, my net worth just passed the A$2m mark. So I'm officially a 'multimillionaire' (for the moment). Just goes to show how little 'millions' are worth these days. I still have a (small) mortgage, I still take a packed lunch to work, and I'm still a 'wage slave' hoping that I don't get retrenched before I reach my planned retirement age (~67-70). As I'll be 'too rich' to qualify for a part-pension or benefits card when I reach retirement age, having a reasonably comfortable retirement will rely on having my mortgage paid off and having retirement savings that (at current interest rates) will generate around $25,000 pa income. Hardly the jet-setting lifestyle the term 'multimillionaire' normally brings to mind? If I do keep my job for another 10-15 years I should be able to build up my retirement savings sufficiently to have an after-tax income in retirement close to my take home pay. One side-benefit of making large salary sacrifice contributions into superannuation is that one is acclimatised to a more modest 'pay packet'.

Subscribe to Enough Wealth. Copyright 2006-2017

Overall, my net worth just passed the A$2m mark. So I'm officially a 'multimillionaire' (for the moment). Just goes to show how little 'millions' are worth these days. I still have a (small) mortgage, I still take a packed lunch to work, and I'm still a 'wage slave' hoping that I don't get retrenched before I reach my planned retirement age (~67-70). As I'll be 'too rich' to qualify for a part-pension or benefits card when I reach retirement age, having a reasonably comfortable retirement will rely on having my mortgage paid off and having retirement savings that (at current interest rates) will generate around $25,000 pa income. Hardly the jet-setting lifestyle the term 'multimillionaire' normally brings to mind? If I do keep my job for another 10-15 years I should be able to build up my retirement savings sufficiently to have an after-tax income in retirement close to my take home pay. One side-benefit of making large salary sacrifice contributions into superannuation is that one is acclimatised to a more modest 'pay packet'.

Subscribe to Enough Wealth. Copyright 2006-2017

Sunday 1 January 2017

Diet & Exercise update - Week0 2017

I managed to avoid overeating too much during the xmas break, so I'm starting 2017 about 10 kg lighter than at the start of 2016 (but about 10 kg more than where I got to mid-way through the year). My best weight was achieved around the time we went skiing and I did the City2Surf last August, but since then I've been very slack about sticking to my diet plan, and the weight has slowly been creeping up again. So far in 2017 I haven't eaten any junk food - so the trick will be to continue that throughout 2017 (and the rest of my life)!

We drove up to the lake house on Christmas Day, and spent a few days relaxing with my parents. The boys there with my parents for a couple more weeks, while DW and I go back to work on Tuesday. We'll drive up again next weekend, and then we'll collect the boys the following weekend and bring them back to Sydney.

I didn't do any target shooting practice or much walking while at the farm - it was too hot to go for long walks in the day, and there were a few too many mosquitos about for a pleasant evening stroll. But I did chop down some lantana and I spent a couple of hours on the tractor slashing one of the paddocks. We also did some gold fossicking in a local state forest (didn't find any gold in the samples of dirt we collected), so at least I got a bit of exercise while at the farm.

As today is the first of Jan I'll make sure I reach my daily step-count goal of 10,000+ steps/day, and also make sure I do my daily 5BX and do some SCATT air pistol training before midnight.

Subscribe to Enough Wealth. Copyright 2006-2017

We drove up to the lake house on Christmas Day, and spent a few days relaxing with my parents. The boys there with my parents for a couple more weeks, while DW and I go back to work on Tuesday. We'll drive up again next weekend, and then we'll collect the boys the following weekend and bring them back to Sydney.

I didn't do any target shooting practice or much walking while at the farm - it was too hot to go for long walks in the day, and there were a few too many mosquitos about for a pleasant evening stroll. But I did chop down some lantana and I spent a couple of hours on the tractor slashing one of the paddocks. We also did some gold fossicking in a local state forest (didn't find any gold in the samples of dirt we collected), so at least I got a bit of exercise while at the farm.

As today is the first of Jan I'll make sure I reach my daily step-count goal of 10,000+ steps/day, and also make sure I do my daily 5BX and do some SCATT air pistol training before midnight.

Subscribe to Enough Wealth. Copyright 2006-2017

Subscribe to:

Posts (Atom)